나는 무언가를 할 때 먼저 실행을 통해 경험해 보는 성향을 가지고 있다. 하지만, 선행된 자료가 있을 때는 이를 최대한 받아들이려고 한다. 특히, 내가 처한 환경과 비슷한 상황에서 성공한 사람 혹은 선행자의 조언이 있다면 반드시 따르려 한다. 나는 그들이 조언하는 “해야 할 것”보다는 “하지 말아야 할 것”을 더 철저하게 지키려고 노력하는 편이다. 어떤 선택을 하든 리스크를 최소화하면서도, 내 방식대로 경험을 통해 배우는 것을 중요하게 생각한다.

예를 들어, 내 인생에 있어서 나와 완전히 동일한 조건의 사람은 없다. 그래서 답이 없는 상황에서도 나는 먼저 실행해 보고, 용기 있게 도전하는 편이다. 그리고 실패하더라도 나를 탓하지 않는다. 나는 단지 “성공으로 가는 한 가지 길을 지웠을 뿐”이라고 생각하기 때문이다.

이제 주식을 예로 들어보자. 주식 투자에 대해서는 이미 수많은 사람들이 선행된 경험과 결과를 책과 강연을 통해 남겼다. 나는 이 점에서 큰 교훈을 얻을 수 있다고 생각한다. 우리의 경제 시스템은 100년 전보다 발전했다. 그러나 주식을 거래하는 측면에서 인간의 본성은 단 1{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374}도 변하지 않았다고 생각한다. 투자에 대한 우리의 반응, 공포와 탐욕, 군중심리, 그리고 비이성적인 행동들은 여전히 반복되고 있다. 단, 기술의 발전으로 인해 더 많은 투자자들이 빠르게 정보를 습득하고, 시장의 경쟁이 더 치열해진 것은 사실이다. 하지만, 그 의미가 모든 투자자가 현명한 선택을 하는 것은 아니다. “우리가 사는 시대는 달라”라고 치부하는 것보다 선행 투자자들의 행동과 환경을 관찰하고, 이해하여 내가 가져가야 할 행동양식을 정리하는 것이 보다 현명한 방식이라고 생각한다.

그래서 주변 사람들이 주식 투자나 다른 형태의 투자를 시작할 때, 나는 최소한의 지식(독서)과 함께 “테스트 투자(몇백만 원 수준)”를 통해 시장에 점진적으로 노출될 것을 추천한다. 이것은 단순한 돈벌이가 아니라, 투자라는 세계를 이해하는 과정이다.

지금부터 소개할 내용은 내가 가진 투자에 대한 생각이다. 이 생각은 내가 직접 창조한 것이 아니라, 위대한 투자자들의 사상과 원칙을 조합하고, 나 나름대로 해석한 “복제된 세계관”이다. 나는 어린 시절 워런 버핏의 추천서 현명한 투자자(The Intelligent Investor)를 읽으며 투자 세계에 입문했다. 이후 벤저민 그레이엄, 필립 피셔, 피터 린치, 하워드 막스, 찰리 멍거, 그리고 워렌버핏의 글과 강연을 통해 기초를 배우고 나만의 경험을 통해서 그 지식들을 유기적으로 연결했다. 그렇게 나는 그들의 “Legacy(유산)”를 따라가고 있다.

아직 자녀는 없지만, 나의 한 가지 로망은 나중에 내 자녀가 초등학교 6학년쯤 되었을 때 나는 이 글과 같은 흐름으로 자녀에게 투자에 대해 설명해주고 싶다. 위대한 투자자들이 남긴 지혜와 내가 경험한 무수한 실패를 전달하면서 조금 실수를 줄이는 방향으로 말이다. 그런 의미에서 내가 책, 인터뷰 등 다양한 곳에서 배웠고 나의 기반이 되어 있는 내용에 대해서 모든 것을 서술해 보았다.

이제부터 소개할 내용은 내가 지금까지 위대한 투자자들에게 간접적으로 배우고, 이해한 투자에 대한 기반이자 전부이다.

What is Investing?

투자란 무엇인가?

먼저, 위대한 투자자들의 정의를 먼저 살펴보자.

벤저민 그레이엄 (Benjamin Graham)

투자는 철저한 분석을 기반으로 원금을 보호하고 적절한 수익을 기대할 수 있어야 한다. 그렇지 않으면 투기다.

An investment operation is one which, upon thorough analysis, promises safety of principal and a satisfactory return. Operations not meeting these requirements are speculative.

필립 피셔 (Philip Fisher)

진정으로 뛰어난 주식을 사서 장기적으로 보유하는 것이 투자다.

Investment is about buying truly outstanding stocks and holding them for the long term.

워런 버핏 (Warren Buffett)

투자는 지금의 소비를 미루고 미래에 더 많은 소비를 하기 위한 과정이다.

Investing is laying out money now to get more money back in the future.

찰리 멍거 (Charlie Munger)

훌륭한 회사를 찾아서 적절한 가격에 사는 것이 투자다.

A great business at a fair price is superior to a fair business at a great price.

하워드 막스 (Howard Marks)

투자는 리스크를 이해하고 통제하는 것이다.

The most important thing is to understand and control risk.

이 다섯 명의 투자 철학은 모두 다르지만, “투자”에 대해서 결국 자본(내가 가진 부)을 효과적으로 운용하여 장기적인 부를 창출하는 것을 목표로 한다. 꽤 직관적이고 심플하다. 정의에 대해서 내가 추가로 언급할 내용은 없다.

Why Should You Invest?

투자를 해야 하는 이유

많은 사람들이 투자에 대해 이야기할 때, 가장 먼저 떠올리는 이유는 “돈을 벌기 위해서”일 것이다. 이제 돈을 벌어야 하는 목적 외에 다른 경제적인 구조에 대해서 언급하고자 한다.

나는 경제학적으로 투자가 필수적인 이유는 아래 2가지가 매우 크게 작용한다고 생각한다.

첫째, 인플레이션(물가 상승)으로 인해 돈의 가치가 지속적으로 하락한다.

우리가 은행에 돈을 그냥 두기만 하면, 시간이 지날수록 그 돈의 구매력은 줄어든다. 10년 전 1,000원이 지금은 800원의 가치밖에 되지 않는다면, 가만히 있는 것만으로도 우리는 손실을 보는 셈이다.

둘째, 돈이 돈을 벌어주는 시스템, 즉 복리(Compounding Effect)를 활용해야 한다.

시간이 지날수록 투자 수익은 기하급수적으로 증가하며, 장기적으로 꾸준히 투자한 사람과 그렇지 않은 사람의 자산 차이는 걷잡을 수 없이 벌어진다. 예를 들어, 연 10{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374}의 수익률로 10년간 투자한다면 원금은 2.6배로 증가한다. 1950년에 S&P 500에 1달러를 투자했다면, 2024년에는 약 1,617달러가 된다.

즉, 투자를 하지 않는 것은 단순한 기회 손실이 아니라, 시간을 낭비하는 것과 같다. 우리는 매일 돈을 벌기 위해 일하지만, 돈이 스스로 일하게 만드는 방법을 배운다면 우리의 삶은 훨씬 더 여유로워질 수 있다.

Why Stocks Among Many Investment Options?

많은 투자방식 중에 왜 “주식”인가?

투자를 고려하는 사람들은 다양한 선택지를 가지고 있다. 부동산, 채권, 암호화폐 등 여러 투자 자산이 존재하지만, 장기적으로 가장 강력한 투자 자산은 주식이라고 생각한다. 이는 단순한 수익률의 문제가 아니라, 주식이 가진 본질적인 특성 때문이다.

1. 주식은 경제 성장의 혜택을 직접 받을 수 있는 자산이다.

경제가 성장하면 기업도 성장하고, 기업이 성장하면 주식의 가치도 상승한다. 워런 버핏은 주식을 “경제 성장의 직접적인 혜택을 받을 수 있는 자산”이라고 정의했다. 이는 주식이 단순한 금융 상품이 아니라, 기업의 일부를 소유하는 것임을 의미한다.

반면, 채권은 정해진 이자를 지급받는 구조로, 기업의 성장과 무관하다. 기업이 아무리 성장하더라도 채권 보유자는 약속된 이자만 받을 뿐이다. 주식은 다르다. 기업의 수익성이 성장할수록 사내에 축적된 현금으로 투자를 하거나, 배당을 한다. 그리고 그에 따라 주가가 상승한다. 그 성장의 혜택을 직접 누릴 수 있다. 따라서 주식은 경제 성장과 함께 수익이 증가하는 생산적 자산(Productive Asset)이다.

2. 주식은 인플레이션을 방어할 수 있는 자산이다.

저축은 시간이 지날수록 화폐 가치가 하락하는 문제를 안고 있다. 인플레이션이 지속되면 동일한 금액으로 구매할 수 있는 재화와 서비스의 양이 줄어들기 때문이다. 부동산은 인플레이션 방어 기능을 갖지만, 유지보수 비용, 세금, 유동성 부족 등으로 인해 투자 효율성이 떨어질 수 있다.

반면, 주식은 인플레이션 환경에서도 기업이 가격을 조정할 수 있기 때문에 자연스럽게 가치가 증가할 가능성이 높다. 기업이 생산하는 제품과 서비스의 가격이 상승하면, 이는 매출 증가로 이어지고 결국 기업 가치 상승으로 반영된다. 주식은 이러한 메커니즘을 통해 장기적으로 인플레이션을 방어할 수 있는 강력한 자산이 된다.

3. 주식은 복리(Compounding)의 효과를 극대화할 수 있다

복리는 시간이 지날수록 투자 수익을 기하급수적으로 증가시키는 핵심 요소다. 찰리 멍거는 “주식 투자자는 시간이 지날수록 복리의 혜택을 받는다”라고 강조했다. 연평균 10{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374}의 수익률로 10년간 투자하면 원금은 2.6배, 20년 후에는 6.7배, 30년 후에는 17.4배로 증가한다. 채권도 복리를 적용할 수 있지만, 이자율이 낮아 효과가 제한적이다. 부동산의 경우 임대료 수익이 있지만, 유지보수 비용과 재투자 비용이 크기 때문에 복리 효과가 상대적으로 적다.

주식은 기업의 이익이 증가하면 주가가 상승하고, 배당금이 증가하며, 이를 다시 재투자하는 구조이므로 복리 효과를 극대화할 수 있는 자산이다. 특히, 장기적으로 투자할 경우 복리의 힘은 더욱 강력해지며, 이는 주식을 장기 투자에 적합한 자산으로 만든다.

4. 주식 투자는 단순한 자산 증식이 아니라, 학습과 성장의 과정이다.

주식 투자는 단순한 돈벌이 수단을 넘어, 투자자가 세상을 더 깊이 이해할 수 있는 기회를 제공한다. 필립 피셔는 “훌륭한 기업에 투자하면, 그들과 함께 배우고 성장할 수 있다”라고 말했다.

주식을 분석하는 과정에서 투자자는 특정 산업과 기업을 연구하게 된다. 예를 들어, 자동차 산업에 관심이 있다면 테슬라, 도요타, 현대차와 같은 기업을 분석하게 되고, 이를 통해 자동차 시장의 흐름과 미래 기술에 대한 이해가 깊어진다. 테크 산업, 헬스케어, 소비재 등 자신이 관심 있는 분야를 연구하는 과정에서 투자자는 경제 전반에 대한 통찰력을 키울 수 있다.

또한, 주식을 보유하는 것은 기업의 일부를 소유하는 것이므로, 기업이 어떤 방식으로 돈을 벌고 성장하는지 자연스럽게 이해하게 된다. 이는 단순한 자산 증식을 넘어, 경제와 시장을 읽는 능력을 키우는 과정이 된다. 따라서, 투자자에게 성장할 수 있는 기회를 부여한다. 나는 만약 4번 요소가 투자에 없었다면, 위대한 투자자 중 많은 사람들이 사라지거나 다른 사람들로 대체되었을 것이라고 생각할 만큼 매우 중요한 요소라고 생각한다.

What Kind of Investor Will You Be?

어떤 투자자가 될 것인가?

투자자들은 기본적으로 시장 평균을 따라갈 것인가, 시장을 이기려 할 것인가라는 선택에 직면한다. 이 선택에 따라 보수적 투자자(Conservative Investor)와 공격적 투자자(Aggressive Investor)로 나뉠 수 있다.

보수적 투자자는 패시브 투자(Passive Investing)를 선택한다. 이들은 시장 수익률을 그대로 받아들이고, 장기적으로 복리 효과를 극대화하는 전략을 따른다.

반면, 공격적 투자자는 액티브 투자(Active Investing)를 선택한다. 이들은 시장을 이기기 위해 개별 종목을 분석하고, 적극적인 매매 전략을 구사한다.

벤저민 그레이엄과 필립 피셔는 방어적(보수적) 투자자와 공격적 투자자를 구분했지만, 그들이 바라본 시각은 차이가 있었다. 그레이엄은 위험 회피와 안전성을 중심으로 투자자를 구분했고, 피셔는 성장성과 장기적 가치 창출을 기준으로 투자자를 나누었다.

이제, 두 관점을 통해 보수적 투자와 공격적 투자의 차이를 살펴보겠다.

벤저민 그레이엄: 리스크 관리 중심의 투자자 유형 구분

벤저민 그레이엄은 “투자의 가장 중요한 목표는 손실을 방지하는 것”이라고 강조했다. 그는 투자자를 보수적 투자자(패시브 투자자)와 공격적 투자자(액티브 투자자)로 나누었으며, 이 구분은 리스크 감수 성향과 수익 기대치의 차이에서 비롯되었다.

방어적 투자자 (패시브 투자자, Conservative Investor)

보수적 투자자는 최대한 안전한 투자를 선호하며, 시장 수익률을 그대로 따라가려는 성향을 가진다. 이들은 변동성이 낮고, 안정적인 자산을 중심으로 포트폴리오를 구성한다.

특징

– 원금 보호가 최우선

– 저평가된 주식 중에서도 재무 건전성이 높은 기업을 선호

– 채권과 배당주 중심의 포트폴리오 구성 (주식 비중이 낮음)

– S&P 500 ETF 등 지수를 추종하는 투자 방식 선호

– 안전마진(Margin of Safety)을 크게 설정

– 단기적인 변동성을 회피하고 장기적으로 복리 효과를 극대화

대표적인 전략

– S&P 500 ETF, 다우존스 ETF 등 지수 투자

– 배당주 투자 및 채권 보유 비중 확대

– 순자산, 순유동자산 등 자산가치에 중심이 된 투자

공격적 투자자 (액티브 투자자, Aggressive Investor)

공격적 투자자는 시장보다 높은 수익을 목표로 하며, 적극적인 종목 발굴과 매매를 실행한다. 이들은 단순히 저평가된 주식을 찾는 것이 아니라, 성장 가능성이 높은 기업을 찾아 높은 수익을 기대한다.

특징

– 더 높은 수익을 위해 일정 부분 리스크를 감수

– 저평가된 기업뿐만 아니라, 시장보다 빠르게 성장하는 기업에 투자

– 성장성이 높은 산업(테크, 바이오 등)에 관심이 많음

– 기업 분석과 시장 흐름을 지속적으로 연구하여 투자 결정

– 단기적인 가격 변동성은 감수하면서도, 철저한 분석을 통해 내재가치가 높은 주식을 선택

대표적 전략

– 개별 주식 직접 투자 및 적극적인 리밸런싱

– 성장 산업(테크, 바이오, 혁신 기업) 중심 투자

– 시장 조정기에 공격적인 저점 매수 전략

필립 피셔: 성장성 중심의 투자자 유형 구분

필립 피셔는 벤저민 그레이엄과는 다른 시각에서 투자자를 나누었다. 그는 단기적인 시장 변동성을 피하는 보수적 투자자가 오히려 더 위험할 수도 있다고 보았다. 그레이엄의 보수적 투자자는 주로 안정적인 배당주, 채권, 우량주를 선호하는 반면, 피셔의 보수적 투자자는 과거 실적에 의존하며, 미래 성장성을 간과하는 투자자였다.

보수적 투자자 (패시브 투자자, Conservative Investor)

특징

- 단기적인 변동성을 피하려 하지만, 장기적인 성장 기회를 놓칠 가능성이 큼

- 배당을 지급하는 안정적인 기업을 선호

- 과거 실적을 지나치게 중요하게 여김

- 기업의 연구개발(R&D), 혁신, 시장 점유율 증가 가능성에 대한 고려 부족

- 기술적 혁신이 부족한 기업에도 투자할 가능성이 높음

공격적 투자자 (액티브 투자자, Aggressive Investor)

특징

- 단순히 저평가된 기업을 찾는 것이 아니라, 미래 성장 가능성이 높은 기업을 발굴

- 장기적으로 훌륭한 기업을 찾아 보유하며 복리 효과를 극대화

- 연구개발(R&D), 시장 점유율 증가, 경영진 역량을 철저히 분석

- 단기 변동성에 흔들리지 않고, 장기적 성장성에 집중

대표적인 전략

- 기술 혁신을 주도하는 기업에 투자

- 경영진이 뛰어난 회사에 투자

- 단기적인 주가 조정보다 장기적 성장성을 우선시

결국, 피셔의 관점에서 보수적 투자자는 지나치게 안정성에 집착하여 큰 기회를 놓칠 위험이 있고,

공격적 투자자는 기업의 성장 가능성을 보고 장기적으로 부를 축적하는 전략을 따른다.

자, 이제 당신은 어떤 투자자가 될 것인가? 먼저 데이터를 살펴보자.

실제 데이터를 살펴보면, 패시브 투자(보수적 투자자)가 장기적으로 액티브 투자(공격적 투자자)보다 높은 성과를 기록하는 경우가 많다. 많은 투자자들은 시장을 이기기 위해 적극적으로 매매하고 특정 종목을 발굴하려 하지만, 장기적으로 이러한 전략이 성공하는 경우는 극히 드물다. 반면, 단순히 시장을 따라가는 패시브 투자자들은 대부분의 액티브 투자자를 능가하는 성과를 내고 있다.

SPIVA(Active vs. Passive Investing) 보고서에 따르면, 10년 동안 액티브 펀드 중 85~90{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374}가 S&P 500을 이기지 못했다. 이보다 긴 20년 동안의 데이터를 분석하면, 95{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374} 이상의 액티브 펀드가 지수를 초과하는 성과를 내지 못했다. 즉, 대다수의 전문 펀드 매니저들조차 시장을 지속적으로 이기는 것이 불가능에 가깝다는 점을 보여준다. 개인 투자자의 경우도 상황은 크게 다르지 않다.

Dalbar Research 보고서에 따르면, 지난 20년간 개별 투자자의 평균 연간 수익률은 3~5{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374} 수준에 불과했다. 같은 기간 동안 S&P 500 지수의 연평균 수익률이 8~10{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374}였음을 고려하면, 개인 투자자는 시장을 이기기는커녕 오히려 장기적으로 상당한 기회비용을 지불하고 있는 셈이다. 이는 감정적인 매매, 시장 타이밍 예측 실패, 과도한 거래 비용 등이 복합적으로 작용한 결과다.

이러한 데이터는 중요한 사실을 시사한다. 보수적인 투자자가 단순히 지수를 따라가는 전략만으로도 전체 투자자의 상위 10~20{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374}에 속할 가능성이 높다. 많은 투자자들이 시장을 이기려 애쓰지만, 오히려 패시브 전략을 유지하는 것이 장기적으로 더 높은 확률로 성공을 보장한다는 것이다. 따라서, 투자 성과를 극대화하려는 개인 투자자라면, 굳이 시장을 초과하려 하기보다 패시브 투자를 통해 꾸준히 복리의 효과를 누리는 것이 가장 효율적인 전략이 될 수 있다.

시장 수익률 관점에서 본 알파(α)와 베타(β) 이론

투자 성과를 분석할 때, 알파(α)와 베타(β) 개념은 투자자의 성향과 전략을 이해하는 데 중요한 역할을 한다.

패시브 투자자는 시장 수익률을 그대로 따르는 것(β=1) 을 목표로 하며, 액티브 투자자는 시장 대비 초과 수익(α>0)을 창출하는 것을 목표로 한다.

1. 베타(β): 시장과 함께 움직이는 정도

베타(β)는 주식이나 포트폴리오가 시장 전체와 얼마나 동조하여 움직이는지를 나타내는 지표다. 이는 투자자의 리스크 감수 성향을 평가하는 중요한 요소다.

- β = 1 → 주식(혹은 포트폴리오)의 수익률이 시장과 동일한 움직임을 보인다.

- β > 1 → 시장보다 더 큰 변동성을 보인다. (예: β = 1.5이면 시장이 10{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374} 상승할 때 주가는 15{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374} 상승)

- β < 1 → 시장보다 변동성이 낮다. (예: β = 0.5이면 시장이 10{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374} 상승할 때 주가는 5{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374} 상승)

- β < 0 → 시장과 반대 방향으로 움직이는 자산 (예: 금, 일부 채권 등)

예를 들어, 테슬라, 넷플릭스 같은 성장주는 β가 1보다 커서(β > 1) 시장보다 더 큰 변동성을 가진다. 반면, 코카콜라, P&G 같은 방어주는 β가 1보다 작아(β < 1) 시장보다 변동성이 낮다. 패시브 투자자(보수적 투자자)는 일반적으로 베타가 1에 가까운(β ≈ 1) 시장 전체를 추종하는 전략을 택한다.

이는 시장 수익률을 따라가면서도, 과도한 리스크를 감수하지 않는 안정적인 방식이다. 반면, 액티브 투자자(공격적 투자자)는 높은 베타(β > 1) 종목을 선호하거나, 시장 변동성을 활용하여 포트폴리오를 조정하려 한다.

2. 알파(α): 초과 수익률 (Active Return)

알파(α)는 포트폴리오의 실제 수익률이 시장(혹은 벤치마크)의 기대 수익률을 초과한 정도를 의미한다.

즉, 투자가 시장을 이겼는지(Positive Alpha) 또는 못 미쳤는지(Negative Alpha)를 나타내는 지표다.

알파(α) 계산 공식:

α=실제수익률−(무위험수익률+β×시장수익률)

- α > 0 → 시장보다 더 높은 수익을 기록 → 초과 수익(Positive Alpha)

- α = 0 → 시장과 동일한 성과

- α < 0 → 시장보다 낮은 수익을 기록 → 저조한 성과(Negative Alpha)

예를 들어, 펀드 매니저가 시장보다 더 높은 수익을 기록하면 긍정적인 알파(α > 0) 를 창출한 것이고, 반대로 시장이 10{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374} 상승했는데 포트폴리오는 8{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374}만 올랐다면 알파(α)는 음수가 된다. 액티브 투자자는 알파(α) 창출을 목표로 하며, 시장 대비 초과 수익을 얻기 위해 노력한다.

그러나, 앞서 언급한 데이터처럼 장기적으로 95{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374} 이상의 액티브 펀드가 시장을 이기지 못한다는 사실을 고려하면, 알파를 지속적으로 창출하는 것이 얼마나 어려운지 알 수 있다. 패시브 투자자는 알파 창출을 목표로 하지 않는다. 대신, 시장 수익률을 그대로 반영하는 전략을 택하고, 장기적으로 복리 효과를 극대화하는 데 집중한다.

자, 이제 선택의 순간이다. 나는 추가적인 기회비용을 감수하고, 나의 시간을 투입하여 액티브 투자를 할 의지가 있는가? 재무제표를 분석하고, 산업의 흐름을 연구하며, 끊임없이 시장을 공부할 각오가 되어 있는가? 사실, 투자에 대한 고민하는 과정 없이, 재무제표에 대한 아무런 이해도 없이 단순히 인덱스 투자만으로도 충분한 수익을 낼 수 있다. 더 나아가, 지수에 투자하는 것만으로도 장기적으로 대부분의 투자자를 능가하는 성과를 거둘 수 있다. 그렇다면, 어떤 선택이 더 효율적일까?

그 답은 각 개인의 성향과 목표에 달려 있다. 만약 이 모든 사실을 인지하고도, 여전히 알파(α)를 추종하는 노력을 하겠다면 다음 설명으로 넘어가도 좋다. 다만, 그 과정에서 요구되는 기회비용이 예상보다 훨씬 클 수도 있다는 점을 반드시 고려해야 한다. 액티브 투자는 단순한 투자가 아니라, 하나의 직업과도 같다는 사실을 잊지 말아야 한다.

Things to Bear in Mind to Become an Aggressive Investor

공격적 투자자가 되기 위해서 감수해야 하는 것들

액티브 투자(공격적 투자)는 시장을 초과하는 수익(알파, α)을 창출하는 것을 목표로 한다. 그러나 이를 위해 투자자가 감수해야 하는 “기회 탐색 비용(Opportunity Seeking Cost)” 이 상당하다.

이 비용은 단순한 금전적 비용뿐만 아니라, 시간과 심리적 스트레스, 그리고 잘못된 판단으로 인한 기회 손실까지 포함된다. 다음은 공격적 투자자가 감수해야 하는 주요 기회 탐색 비용을 정리해 보았다.

1. 정보 탐색 비용 (Research Cost)

좋은 투자 기회를 찾기 위해서는 엄청난 시간과 노력이 필요하다. 공격적 투자자는 단순히 시장을 따라가는 것이 아니라, 개별 종목을 발굴해야 한다. 이는 필연적으로 기업 분석, 산업 연구, 재무제표 검토, 경쟁사 비교 등의 과정을 요구한다.

이 과정에서 투자자는 다음과 같은 부담을 안게 된다.

- 기업의 실적 보고서, 10-K(사업보고서), 재무제표를 분석하는 데 상당한 시간이 소요된다.

- 특정 산업의 트렌드, 경쟁구도, 혁신 가능성을 연구해야 한다.

- 시장 뉴스, 애널리스트 보고서, 투자자 컨퍼런스를 지속적으로 모니터링해야 한다.

- 공격적 투자자는 많은 시간을 들여 투자 기회를 찾지만, 그 비용이 초과 수익을 보장하지는 않는다.

2. 거래 비용 (Transaction Cost)

매매가 많을수록 수수료와 세금이 쌓인다. 공격적 투자자는 시장 변동성에 대응하기 위해 빈번한 매매를 수행하는 경향이 있다. 하지만 잦은 매매는 거래 비용을 증가시키며, 예상보다 큰 손실을 초래할 수 있다.

- 주식 거래 수수료, 스프레드비용(Bid-Ask Spread) 발생

- 양도소득세 및 거래세 부과 (특히, 단기 매매 시 세금 부담 증가)

- 빈번한 매매로 인해 포트폴리오 수익이 지속적으로 갉아먹힐 가능성

- 특히, 고빈도 매매(흔히, 단타)(High-Frequency Trading) 전략을 활용하는 투자자의 경우, 거래 비용이 급증할 수 있으며, 이를 극복할 만큼의 초과 수익을 내는 것이 쉽지 않다.

3. 감정적 스트레스 비용 (Emotional Cost)

공격적 투자자는 항상 시장을 신경 쓰고, 심리적 압박을 받는다. 액티브 투자자는 시장의 변동성을 직접 경험해야 하며, 이는 감정적인 스트레스와 심리적 압박을 초래할 수 있다.

- 급락장에서 공포 매도(Fear Selling) 를 하거나

- 급등장에서 놓치는 것에 대한 두려움(FOMO, Fear of Missing Out) 으로 비이성적인 매수를 할 가능성이 높다.

- 하루 종일 시장을 모니터링해야 하는 부담감이 커진다.

- 감정적 스트레스는 결국 비효율적인 투자 결정을 유발할 가능성이 높다.

- 특히, 감정적 매매를 반복하면 장기적인 복리 효과를 극대화하는 데 걸림돌이 될 수 있다.

4. 오판 비용 (Misjudgment Cost)

열심히 분석해도 틀릴 수 있다. 액티브 투자자는 특정 종목이나 산업이 급등할 것이라고 예측하고 투자하지만, 그 예측이 틀릴 경우 큰 손실을 볼 가능성이 높다.

- 기업의 미래 성장을 예측하는 것은 본질적으로 어렵다.

- 잘못된 타이밍에 매수하는 경우(Timing Risk), 투자 성과에 치명적인 영향을 미칠 수 있다.

- 복잡한 전략을 구사하지만, 오히려 단순한 인덱스 투자보다 낮은 수익을 기록할 수도 있다.

- 결국, 아무리 뛰어난 투자자라도 모든 판단이 옳을 수 없으며,

- 잘못된 투자 결정이 누적되면 시장을 이기기는커녕 손실을 볼 가능성이 커진다.

5. 유동성 위험 비용 (Liquidity Risk Cost)

유동성이 낮은 자산에 투자하면, 필요할 때 현금화가 어려울 수 있다. 공격적 투자자는 고성장 산업, 중소형주, 신생 기업 등 유동성이 낮은 종목을 선호하는 경우가 많다. 하지만 이러한 자산들은 시장이 좋지 않을 때 쉽게 현금화할 수 없다는 리스크를 동반한다.

- 경기 침체 시, 주식을 팔고 싶어도 매수자가 부족할 수 있다.

- 특정 산업(예: 바이오테크, 스타트업)에서는 유동성이 급격히 낮아질 위험이 있다.

- 급격한 유동성 위기로 인해 자산 가치가 폭락할 가능성이 있다.

- 시장이 좋지 않을 때 현금화가 어려울 수 있다.

6. 자본 기회비용 (Opportunity Cost of Capital)

공격적으로 투자하다가 오히려 지수 투자보다 낮은 성과를 낼 수도 있다. 공격적 투자자는 개별 종목을 선택하며 높은 수익을 기대하지만, 장기적으로 보면 인덱스 투자(S&P 500, ETF)보다 낮은 성과를 기록할 가능성이 높다.

- 연구에 따르면, 장기적으로 시장을 초과하는 투자자는 10~20{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374}에 불과하다.

- 대부분의 투자자는 시장을 이기려고 노력하다가, 오히려 평균 이하의 성과를 기록한다.

What Are Stocks? How Should You View a Business?

주식은 무엇인가? 어떻게 사업을 바라보아야 하는가?

워런 버핏이 말한 이 문장은 단순한 투자 조언이 아니다. 이는 투자를 바라보는 근본적인 태도를 바꿔야 한다는 철학적인 메시지다. 많은 사람들은 주식을 “단순한 숫자, 차트, 가격 변동” 으로만 본다. 하지만 버핏은 “주식은 단순한 티커(symbol)가 아니라, 실제 기업의 일부(ownership)다” 라고 강조한다.

즉, 주식을 사는 것은 “단기적으로 오를 것 같은 숫자를 사는 것이 아니라, 실제로 운영되는 사업의 한 부분을 소유하는 것” 이다.

예시를 하나 들어보겠다.

어느 날, 나는 작은 김밥 사업을 시작하기로 했다. 아침마다 사무실이 밀집한 지역에서 김밥을 판매하는 것이다. 매일 아침, 나는 신선한 재료를 준비해 김밥을 만들고, 출근길 직장인들에게 김밥을 판매한다. 김밥 한 줄의 가격은 1,000원이며, 하루에 약 10줄을 팔 수 있다. 이렇게 하루에 10,000원의 매출을 올리지만, 실제로 내 손에 남는 돈은 매출과는 다르다.

김밥을 만들기 위해서는 재료비가 필요하다. 밥, 김, 계란, 시금치, 단무지 같은 기본 재료를 구매하는 데 김밥 한 줄당 500원이 든다. 10줄을 만들기 위해서는 5,000원의 재료비가 필요하다. 또한, 김밥을 팔기 위해 매일 지하철을 타고 사무실 근처로 이동해야 하는데, 교통비로 하루 100원이 든다. 김밥을 사는 손님들 중에는 카드 결제를 선호하는 사람이 많아서, 카드 결제 수수료도 고려해야 한다. 하루에 200원 정도의 카드 결제 수수료가 발생한다.

이렇게 비용을 다 계산하고 나면, 하루에 내 손에 남는 돈, 즉 순이익은 1,500원이다. 하루 1,500원의 순이익을 번다면, 한 달이면 약 45,000원 가량이고, 1년(365일)이면 약 547,500원의 순이익을 얻을 수 있다.

그런데 나는 이 사업을 더 키우고 싶었다. 김밥 종류를 다양하게 늘리고, 하루 판매량을 20줄, 30줄로 늘리고 싶었다. 하지만 이를 위해서는 초기 투자금이 필요했다. 더 많은 재료를 사기 위해 비용이 필요하고, 좋은 위치에서 장사를 하려면 임대료도 고려해야 했다. 그래서 나는 투자자를 모집하기로 했다.

투자자를 모집한다는 것은 곧 내 사업의 일부를 판매한다는 의미다. 투자자들은 내 김밥 사업에 돈을 투자하고, 그 대가로 내 사업의 일부를 소유하게 된다. 그렇다면, 투자자들은 내 사업의 주식을 얼마에 사고 싶을까?

이 사업이 매년 54만 원의 순이익을 꾸준히 창출한다면, 단순하게 계산하면 5년 동안 약 270만 원의 이익을 낼 수 있다. 그렇다면 투자자들은 이 김밥 사업을 270만 원에 살 의향이 있을까? 아니면, 사업이 더 성장할 가능성을 보고 더 높은 가격을 지불할 수도 있을까?

하지만 반대로, 이 사업이 반드시 성공할 것이라는 보장은 없다. 만약 사람들이 더 이상 김밥을 사지 않는다면? 혹은 경쟁자가 나타나서 나보다 더 저렴하고 맛있는 김밥을 판다면? 재료비가 올라가서 수익이 줄어든다면? 이런 위험 요소들을 고려하면, 투자자들은 내 주식을 싸게 사고 싶어질 것이다.

이러한 과정이 바로 주식 투자의 본질이다. 주식은 단순한 숫자가 아니라, 실제 사업을 이해하고 그 가치를 평가하는 과정이다. 투자자는 주식을 살 때 단순히 차트와 숫자를 보는 것이 아니라, 기업이 어떻게 돈을 벌고, 미래에 성장할 수 있는지를 분석해야 한다.

결국, “어떤 주식을 사야 하는가?” 라는 질문은 “어떤 사업을 소유하고 싶은가?” 라는 질문과 같다. 주식을 사는 것은 단순한 가격 변동을 추측하는 것이 아니라, 기업의 일부를 소유하는 것이다. 투자자는 자신이 투자하는 기업이 어떻게 돈을 벌고, 어떤 성장 가능성이 있으며, 어떤 위험을 가지고 있는지를 깊이 이해해야 한다. 이 원칙을 이해한다면, 우리는 보다 현명한 투자 결정을 내릴 수 있을 것이다.

다음은 버핏이 주주서한에서 예시로 들었던 예시이다.

“손 안의 새 한 마리가 덤불 속의 두 마리보다 낫다”

내재 가치는 오래전부터 논의되어 온 개념이다. 사실, 가장 먼저 이 개념을 제시한 사람은 이솝(Aesop, 이솝우화의 저자)이라고 볼 수 있다. 그가 600년경 BC에 말했던 “손 안의 새 한 마리가 덤불 속의 두 마리보다 낫다(A bird in the hand is worth two in the bush)”라는 격언이 바로 그 본질을 담고 있다.

즉, 지금 당장 확실한 돈(손 안의 새 한 마리)이 미래에 얻을 수 있는 불확실한 돈(덤불 속의 두 마리)보다 더 가치 있을 수 있다는 것이다. 중요한 것은 미래의 현금 흐름이 얼마나 확실한가?, 그 덤불이 얼마나 멀리 있는가?, 미래의 이자율(할인율)은 어떻게 변할 것인가?와 같은 질문에 대한 답을 찾는 것이다.

우리는 수많은 기업들을 검토하면서, 각 기업이 미래에 몇 마리의 새(현금 흐름)를 줄 수 있을지 평가한다. 그리고 우리가 “구매할 덤불”을 결정하는 과정이다.

투자를 할 때 가장 먼저 던져야 할 질문은 “이 주식이 비싼가, 싼가?” 가 아니다. 대신 “이 주식의 본질적인 가치는 얼마이며, 현재 시장 가격과 비교했을 때 저평가되었는가?” 를 고민해야 한다. 주식 시장에서는 가격(Price)과 가치(Value) 가 항상 일치하지 않는다.

워런 버핏은 말했다. “가격은 우리가 지불하는 것이고, 가치는 우리가 얻는 것이다.” 즉, 가격은 단기적으로 시장의 감정과 심리에 의해 흔들리지만, 장기적으로는 기업의 본질적인 가치가 주가에 반영된다는 믿음이 있다. 따라서 투자자는 단순히 현재 가격이 싸 보인다고 매수하는 것이 아니라, 해당 기업의 내재가치보다 저렴한 가격에 거래되고 있는지를 분석해야 한다.

“내재가치”란 무엇인가?

What Is Intrinsic Value?

내재가치(Intrinsic Value)란?

내재가치는 그 자산이 본질적으로 가지고 있는 실제 가치이다. – 워렌버핏

벤저민 그레이엄은 내재가치를 수학적으로 명확하게 정의하지는 않았지만, 그 개념은 “개인 사업을 사는 것과 동일한 방식으로 기업을 평가해야 한다” 는 철학에 가깝다. 내재가치는 단순한 주가 변동이 아니라, 기업이 벌어들이는 모든 현금 흐름(Cash Flow)의 현재 가치로 정의할 수 있다.

즉, 만약 미래를 완벽하게 예측할 수 있다면, 기업이 앞으로 벌어들일 모든 돈을 현재 가치로 환산한 것이 내재가치가 된다. 하지만 현실적으로 미래를 100{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374} 예측하는 것은 불가능하기 때문에, 투자자들은 다양한 방법을 사용하여 내재가치를 추정한다.

내재가치와 시장 가격의 차이

기업의 내재가치와 시장에서 거래되는 주가는 항상 일치하지 않는다. 그렇기 때문에 투자자는 기업이 내재가치보다 낮은 가격에 거래될 때 매수하고, 내재가치에 도달할 때까지 기다리는 전략을 취해야 한다.

내재가치(Intrinsic Value)의 특징

- 기업의 보유 자산, 이익 창출 능력, 현금흐름, 성장 가능성을 종합적으로 평가하여 결정되는 객관적인 가치

- 시장의 감정(공포와 탐욕)에 의해 변하지 않는 본질적인 가치

시장 가격(Market Price)의 특징

- 주식 시장에서 실시간으로 변동하는 가격

- 투자자들의 심리, 수급, 뉴스, 금리 변화 등에 따라 급변하는 숫자

- 시장은 단기적으로 감정적인 가격 형성을 하지만, 장기적으로는 기업의 실적과 내재가치에 맞게 가격이 조정된다.

투자자들은 기업을 분석하는 방식에서 크게 두 가지 관점을 가질 수 있다.

첫째, 기업의 현재 재무 상태와 내재 가치를 철저히 분석하여 저평가된 주식을 찾는 방법.

둘째, 기업의 질적 요소와 장기적인 성장 가능성을 분석하여 미래에 크게 성장할 회사를 찾는 방법.

이 두 가지 접근법을 대표하는 인물이 바로 벤저민 그레이엄(Benjamin Graham) 과 필립 피셔(Philip Fisher) 이다. 그레이엄은 철저한 숫자 기반의 분석을 강조했고, 피셔는 기업의 질적 요소와 성장 가능성을 중시했다. 두 사람의 투자 철학은 다르지만, “투자는 현재의 가격과 미래 가치를 비교하는 과정” 이라는 점에서는 동일했다. 그럼에도 불구하고, 어떤 방식이 더 나은지는 여전히 투자자의 선택에 달려 있다. 버핏의 예를 가져온다면 벤그레이엄은 담불 안에 새가 정말로 존재하는지에 대해서 집중했다면, 필피셔는 그 담불 안에 새가 얼마나 늘어날 것인지에 대해서 중요하게 생각했다는 점이다.

그레이엄 vs. 피셔: 어떤 접근법이 더 나은가? 그레이엄과 피셔의 투자 철학은 크게 다르지만, 어느 한 쪽이 절대적으로 옳다고 단정 짓기는 어렵다. 하지만 많은 부분에서 증명된 것은 벤그레이엄의 방식은 규모가 큰 투자에서는 통용되기 어렵다는 것이 주된 중론인 것 같다.

나는 처음에는 벤저민 그레이엄의 영향을 강하게 받아서 양적 분석(quantitative factors)을 중시했다. 하지만 찰리 멍거(Charlie Munger)는 내게 그것만으로는 부족하다고 했다. 그는 법률을 통해 배운 것이 금융 공부보다 더 많다고 했으며, 투자에서도 질적 요소를 더 고려해야 한다고 강조했다. 결과적으로, 나는 찰리와 필립 피셔의 의견이 옳다는 것을 깨달았다.

워렌버핏

할인율(Discount Rate)

내재가치를 구할 때 “이자”에 대한 부분을 언급했다. 미래의 현금을 현재가치로 계산하는데 있어서 이자율은 매우 중요하다. 내가 업무로 담당하는 곳에서의 할인율에 대해서 설명하자면 매우 복잡하지만 일단 어려운 설명을 떠나서 많은 사람들이 워렌에게 할인율은 몇 퍼센트를 사용하는지에 대해서 종종 물어본다. 그 대답은 다음과 같다.

우리는 내재 가치를 평가할 때 장기 무위험 금리(long-term risk-free rate, 즉 정부 채권 금리)을 기준으로 할인율을 정한다. 이는 안전한 투자 자산(예: 미국 국채)의 수익률을 기준으로 기업의 미래 현금 흐름을 현재 가치로 환산하는 방식이다.

워렌버핏

그런데, 나는 중요한 시사점은 단순히 미국 장기채 금리를 사용하는 것이 아니라고 생각한다. 정작 중요한 말은 다음과 같은 언급을 주요하게 생각해야 한다.

우리는 단순히 “한 발짝만 넘으면 되는 1피트 높이의 장애물(One-foot bars)”을 찾아서 넘는다. 우리는 7피트 장애물(Seven-foot bars)을 뛰어넘을 능력이 없지만, 최소한 “이 장애물이 1피트인지, 7피트인지”는 판단할 수 있다.

워렌버핏

내가 생각하는 버크셔의 내재가치를 구하는 방식은 할인율을 미세하게 조정하여 답이 애매하게 오고가는 의사결정에 대해서는 하지 않는다 라는 점이다. 예전 주주총회에서 버핏은 DCF 자체의 계산 방식을 머리 속에 가지고 있지만 어떤 스텝(직원)도 그걸 실제로 계산하거나 하지는 않는다라고 했다. 우리가 생각해야 할 것은 워렌버핏이 8{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374}의 할인율을 적용하는지, 9{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374}를 적용하는지가 아니라 그런 의사결정에서 멀어지는 것이라는 점이다.

내재가치 계산방식의 예시

Example of Intrinsic Value Calculation Methods

다음은 워렌버핏이 주주총회 중 내재가치를 구하는 방식에 대해서 가장 구체적으로 설명한 방식이다. 이를 정리해두었다. 어떤 유명한 투자자들 보다 가장 구체적인 내재가치 계산방식의 Framework를 가르쳐 주었다고 생각한다.

농장(Farm)을 예로 든 내재 가치 평가 방식우리가 농장을 사려고 한다고 가정해 보자.

- 우리가 조사한 결과, 1에이커당 120부셸(bushels) 옥수수 또는 45부셸 대두(soybean)를 생산할 수 있다.

- 우리는 비료 비용(fertilizer costs), 재산세(property taxes), 농부에게 지불할 인건비 등을 알고 있다.

- 이를 보수적으로 계산하면, 소유주(owner) 입장에서 아무 일도 하지 않고 1에이커당 $70의 수익을 얻을 수 있다고 가정한다.

그렇다면, 우리는 이 1에이커당 $70의 수익을 위해 얼마를 지불해야 할까?

- 농업 생산성이 점차 향상될 것인지?

- 농산물 가격이 오를 것인지?

이런 요소를 보수적으로 고려해야 한다.

이제, 우리는 목표 수익률(target return)을 정해야 한다.

- 만약 7{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374} 수익률을 원한다면, 우리는 1에이커당 $1,000을 지불할 수 있다.

- 만약 농지 가격이 1에이커당 $900라면, 우리는 매수를 고려할 것이다.

- 반면, 1에이커당 $1,200라면, 우리는 다른 투자 기회를 찾아볼 것이다.

우리는 기업을 “법인 농장(Corporate Farm)”처럼 평가한다 우리가 기업을 평가할 때도 농장을 평가하는 방식과 동일한 접근법을 사용한다. 이를 위해 우리는 다음을 평가해야 한다.

- 기업의 경쟁력(Competitive Position)

- 이 기업이 앞으로도 시장에서 우위를 유지할 수 있는가?

- 사업의 역학(Dynamics of the Business)

- 이 산업이 장기적으로 어떤 변화를 겪을 것인가?

- 미래 전망(Outlook for the Future)

- 우리는 미래를 얼마나 멀리 내다볼 수 있는가?

그러나, 일부 기업들은 미래를 예측하는 것이 거의 불가능하다. 우리는 미래를 비교적 확신할 수 있는 기업들만을 투자 대상으로 삼아야 한다.

Which Company Should You Invest In?

어떤 기업에 투자할 것인가?

기업을 평가할 때 가장 핵심적인 질문은 내가 투입한 현금이 언제, 얼마나 많은 금액으로 돌아오는가?이다. 테슬라, 맥도날드, 엔비디아 등 어떤 기업을 매수하든, 투자의 본질은 결국 현금 흐름을 예측하고, 그에 대한 대가를 적절히 평가하는 것에 있다. 기업을 하나의 자산으로 바라볼 때, 가장 중요한 요소는 다음과 같다.

- 추가적인 자본 투입이 필요한가?

- 언제부터 현금이 유입되는가?

- 그 현금의 가치는 현재 얼마인가? (적절한 할인율은 얼마인가?)

이 세 가지 질문에 대한 답을 찾아야만 투자자로서 합리적인 결정을 내릴 수 있다.

기업의 현금 흐름이 곧 채권의 이자와 같다. 기업이 향후 벌어들일 현금 흐름은 채권의 이자와 비슷한 역할을 한다. 채권의 경우, 투자자는 일정한 금액을 투자하고, 그 대가로 정해진 기간 동안 일정한 이자를 지급받는다.

하지만 기업은 채권과 다르게 투자자가 직접 미래의 현금 흐름을 예측해야 한다는 점에서 차이가 있다. 어떤 기업의 미래 수익이 안정적이라면, 그 기업은 마치 고정금리가 있는 채권처럼 작용할 것이다. 반면, 기업의 미래 현금 흐름이 불확실하다면, 그것은 투자자가 추가적인 리스크를 감수해야 하는 투자 대상이 된다.

우리는 사업을 이해하고 예측 가능한 기업에만 투자해야 한다. 투자의 핵심은 단순히 *이 기업이 좋은 기업인가?”가 아니다. “이 기업이 앞으로도 꾸준한 현금 흐름을 창출할 것인가?”를 분석하는 것이 더 중요하다.

모든 기업의 내재 가치를 정확히 계산할 수는 없다. 하지만 우리가 잘 이해하고 있는 기업에 대해서는 대략적인 범위를 추정할 수 있다. 즉, 우리는 완벽한 숫자를 도출하는 것이 아니라, 합리적인 오차 범위 내에서 투자 결정을 내리는 것이 목표다.

- 어떤 기업이 10년, 20년 후에도 지속적으로 수익을 창출할 가능성이 있는가?

- 현금 흐름이 꾸준하고 예측 가능한가?

- 투자자가 기업의 미래를 어느 정도 신뢰할 수 있는가?

워렌버핏의 투자 포트폴리오를 보면 브랜드, 소비재 기업들이 다수 존재한다. 그 인수한 이유에 대해서 언급한 적이 있다. 그가 투자한 이유를 다음과 같이 설명한다.

질레트(Gillette) 면도날: 전 세계 면도기 시장의 70{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374}를 차지하고 있다. 100년이 지나도 여전히 강력한 브랜드다. 면도날이 어떻게 만들어지는지, 철강을 어디서 사는지, 유통이 어떻게 이루어지는지는 다 알려진 사실이지만, 여전히 70{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374}를 차지하는 이유는 사람들이 쉽게 브랜드를 바꾸지 않기 때문이다.

코카콜라(Coca-Cola): 연간 190억 케이스가 팔린다. 사람들이 10년 후에도 코카콜라를 마실까? 나는 이 질문에 내 인생을 걸 수 있다.

See’s Candy: 캘리포니아에 3500만 명이 살고 있다. 그들 대부분이 See’s Candy에 대한 기억을 가지고 있다. 초콜릿 시장에서 10년 전에도 스니커즈(Snickers)가 1위였고, 20년 전에도 그랬다. 사람들은 초콜릿을 쉽게 바꾸지 않는다.

How to Make Investment Decisions?

어떻게 투자 의사결정을 할 것인가?

찰리멍거

우리는 모든 기업을 평가할 필요가 없다

우리는 모든 기업을 평가할 수 있는 시스템을 가지고 있지 않다.

대부분의 기업들은 너무 복잡하거나 예측이 어려우므로,

우리는 거의 모든 기업을 “너무 어려운(To Hard)” 범주에 넣고 그냥 포기한다.우리가 하는 일은 단순한 것들을 걸러내는 과정이다.

즉, 쉽게 판단할 수 있는 몇 개의 투자 기회를 찾는 것이다.만약 당신이 “모든 투자 기회를 정확히 평가하는 능력”을 원한다면, 우리는 그런 도움을 줄 수 없다.

투자는 모든 기회들을 고려하여 자신에게 가장 적합한 선택을 하는 과정이다. 버크셔의 주총회나 투자자의 강연에서 “내재가치를 어떻게 구하나요?” 라는 질문은 빠지지 않고 등장한다. 많은 사람들은 투자를 수학 문제처럼 풀 수 있는 단순한 공식이 있을 것이라고 기대한다. 그러나 워런 버핏, 찰리 멍거, 하워드 막스 같은 위대한 투자자들은 이런 질문을 받을 때마다 답답함을 느꼈을 것이라고 생각한다.

왜냐하면, 내재가치는 단순한 숫자가 아니라, 복합적인 사고의 결과라고 생각하기 때문이다. 많은 사람들이 투자에서 “정확한 숫자”를 원한다. 하지만, 현실에서는 단 하나의 정확한 공식으로 내재가치를 구하는 것은 불가능하다.

- 내재가치는 기업의 현재 수익, 미래 성장 가능성, 경제적 해자(Moat), 경영진의 역량, 시장 환경 등 여러 요소를 종합적으로 고려해야 한다.

- DCF(할인된 현금흐름), P/E, P/B 같은 지표는 참고 자료일 뿐, 절대적인 답을 제공하지 않는다.

- 수학적 모델을 맹신하면 오히려 투자에서 위험할 수 있다.

“완벽한 모델은 존재하지 않는다. 하지만 대충 맞는 모델이 완전히 틀린 모델보다는 낫다.”

존 메이너드 케인즈

케인즈의 말처럼, 투자자들도 완벽한 모델이 없다는 것을 인정해야 한다. 투자는 불확실성을 다루는 과정이며, 정확한 답이 아니라 “가장 합리적인 판단”을 내리는 것이 중요하다. 우리의 목표는 복잡한 공식이 아니라, 복잡한 사고방식을 가지는 것이다. 수학적으로 내재가치를 구하는 공식이 있다면, 모든 사람이 부자가 될 것이다. 하지만 현실은 그렇지 않다. 투자는 단순한 수식이 아니라, 논리적 사고와 경험을 바탕으로 한 의사결정의 결과다.

언제 투자해야하는가?

When Should You Invest?

나는 주식 시장 사이클에 대해서는 하워드 막스의 설명이 가장 적합한 설명이라고 생각한다. 특히, 하워드는 재무적인 요소보다도 사람의 심리를 가지고 주식시장에 대해서 해석한다.

주식 시장은 감정에 의해 움직인다. 탐욕과 공포는 투자자들의 판단을 왜곡하며, 이 두 감정이 극단적으로 치닫을 때 시장은 과열되거나 침체된다. 대부분의 투자자들이 낙관적일 때 시장은 이미 고점에 도달했을 가능성이 크고, 반대로 모두가 비관적일 때는 저평가된 기회가 많아진다. 따라서 투자자는 군중심리를 거스르고, 시장이 감정적으로 움직일 때 냉정한 태도를 유지해야 한다.

투자를 조심해야 할 때: 군중심리가 과도하게 낙관적일 때

시장이 과열될 때 투자자들은 비이성적으로 낙관적인 태도를 보인다. 투자에 대한 경계심이 사라지고, 모든 사람이 시장에 뛰어든다. 주식 시장이 단기적으로는 계속 오를 것이라는 믿음이 확산되며, 투자자들은 안전마진을 고려하지 않는다.

군중심리가 과도하게 낙관적인 시기의 특징은 몇 가지 공통점을 가진다.

첫째, 시장 참여자들이 급증한다. 주식 투자에 대한 관심이 높아지고, 경험이 부족한 개인 투자자들이 적극적으로 시장에 뛰어든다. “누구나 돈을 벌고 있다”는 분위기가 형성되며, 주변에서 “지금이 기회다”라는 말이 자주 들리기 시작한다.

둘째, “이번에는 다르다”는 논리가 등장한다. 기존의 투자 원칙이 무시되며, 새로운 패러다임이 시장을 지배한다는 주장이 나온다. 과거 닷컴 버블 당시에는 “인터넷 기업은 수익이 없어도 된다”는 논리가 있었고, 부동산 버블 때는 “부동산 가격은 절대 떨어지지 않는다”는 믿음이 퍼졌다.

셋째, 기업 실적과 무관하게 주가가 급등한다. 수익을 내지 못하는 기업도 높은 가치를 인정받으며, 실적보다 기대감이 주가를 끌어올린다. 시장이 기본적인 기업 분석을 무시하고 단기적인 흐름에만 집중할 때, 거품이 형성될 가능성이 크다.

넷째, 투자자들이 FOMO(Fear of Missing Out, 기회를 놓칠 것 같은 두려움)에 사로잡힌다. 뉴스와 소셜미디어에서는 “지금이 아니면 늦는다”는 메시지가 확산되며, 사람들은 검증되지 않은 정보에도 쉽게 휩쓸린다.

마지막으로, 레버리지가 과도하게 증가한다. 빚을 내서 투자하는 사람들이 많아지고, 신용거래가 폭증한다. 시장이 상승할 때는 큰 수익을 낼 수 있지만, 하락하기 시작하면 급격한 청산이 발생하며 시장 변동성이 커진다.

이런 시기에는 투자 속도를 늦추고 보수적인 접근이 필요하다. 군중심리가 시장을 밀어올리는 동안에도 기업의 내재가치를 평가하고, 가격이 가치보다 과도하게 높은 주식을 피하는 것이 중요하다.

투자 기회는 언제 오는가? 군중심리가 과도하게 비관적일 때

반대로, 시장이 극단적으로 비관적일 때는 저평가된 투자 기회가 나타난다. 대부분의 사람들이 시장에서 도망칠 때가 오히려 가장 좋은 매수 타이밍이 될 수 있다.

첫째, 모든 뉴스가 부정적으로 변한다. 경기 침체, 실업 증가, 금리 인상 등 시장에 대한 부정적인 전망이 쏟아진다. “주식 시장은 끝났다”는 말이 자주 들리며, 투자자들은 시장의 회복 가능성을 낮게 평가한다.

둘째, 투자자들이 극단적인 공포를 느낀다. 공포지수(VIX)가 급등하고, 기관 투자자들이 대량 매도를 하며, 개인 투자자들은 패닉셀링을 한다. 시장이 비이성적으로 하락할 때, 감정적으로 대응하는 투자자들은 손실을 피하기 위해 서둘러 매도한다.

셋째, “주식 시장은 다시는 회복되지 않을 것”이라는 말이 나온다. 투자자들은 장기적인 시장 회복을 의심하고, 주식보다 현금을 보유하는 것이 안전하다고 생각한다. 과거 금융위기 이후, 시장이 저점에 도달했을 때 이런 분위기가 퍼졌다.

넷째, 대규모 청산과 파산이 발생한다. 레버리지를 사용한 투자자들이 강제 청산을 당하고, 일부 기업이나 펀드가 파산한다. 이러한 상황이 발생할 때 시장은 단기적으로 크게 흔들리지만, 장기적인 관점에서는 저가 매수의 기회가 될 수 있다.

역사적으로 가장 좋은 투자 기회는 극단적인 공포 속에서 나타났다. 금융위기 이후 시장이 회복될 때, 코로나 팬데믹 초기의 급락 이후 반등할 때, 비슷한 패턴이 반복되었다. 그러나 군중심리가 극도로 부정적인 상황에서도 기업의 내재가치를 신중하게 평가하는 것이 중요하다. 단순히 가격이 낮다고 해서 투자하는 것이 아니라, 가치 대비 가격이 저렴한지 분석하는 과정이 필요하다.

군중심리와 멀티플 변화의 관계

군중심리는 시장의 멀티플 변화와 밀접한 관계가 있다.

- 군중심리가 긍정적일 때 → 시장의 멀티플이 높아짐 → 고평가된 주식 증가 → 조심해야 할 시점

- 군중심리가 부정적일 때 → 시장의 멀티플이 낮아짐 → 저평가된 주식 증가 → 장기적 투자 기회

시장에 참여하는 투자자들은 단기적인 감정 변화에 휩쓸릴 가능성이 크다. 그러나 군중심리가 극단으로 치닫을 때, 반대로 움직이는 것이 장기적으로 더 나은 투자 성과를 가져올 수 있다.

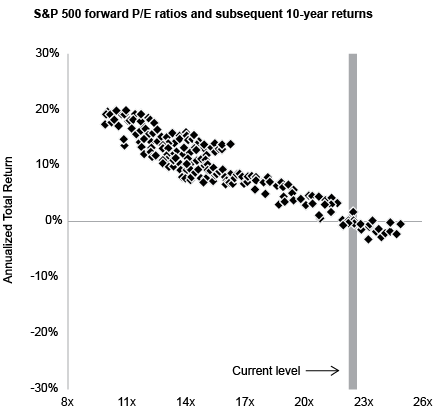

이 그래프는 S&P 500의 선행 주가수익비율(Forward P/E Ratio)과 이후 10년 동안의 연평균 총수익률(Annualized Total Return) 간의 관계를 보여준다. 그래프는 명확한 음의 상관관계를 나타내며, P/E 비율이 낮을수록 향후 10년간의 기대 수익률이 높고, 반대로 P/E 비율이 높을수록 장기 수익률이 낮아지는 경향을 보인다. 현재 시장 수준은 약 23배의 P/E 수준에 위치해 있으며, 이는 역사적으로 낮은 미래 수익률을 의미할 가능성이 크다. 즉, 현 시장에서는 높은 밸류에이션으로 인해 기대할 수 있는 장기 수익률이 상대적으로 낮을 수 있으며, 투자자는 신중한 접근이 필요하다는 시그널로 해석할 수 있다.

통계적인 결과로 역사적 사이클을 무시할 수 없고, 우리는 시장의 사이클에 신중하게 접근해야 한다. 하지만, 이 마저도 언제 어떤 사이클이 올지 알 수 없다는 점이 포인트다.

레버리지(대출) 투자에 대한 생각

Thoughts on Leverage (Debt) Investing

레버리지는 투자 수익을 극대화할 수 있는 강력한 도구지만, 동시에 돌이킬 수 없는 손실을 초래할 수 있다. 워런 버핏과 찰리 멍거는 수십 년간의 투자 경험을 바탕으로 레버리지를 사용하지 않는 것이 장기적인 투자 성공의 필수 요소라고 강조했다. 그들은 레버리지가 단기적으로는 이익을 증폭시키지만, 장기적으로는 예측할 수 없는 시장 변동성을 감당할 수 없게 만든다고 보았다.

레버리지는 좋은 투자자도 망하게 만든다.

레버리지는 투자자에게 감당할 수 있는 것보다 더 큰 포지션을 가지게 만든다. 주가가 상승할 때는 수익이 극대화되지만, 반대로 하락할 때는 손실도 기하급수적으로 커진다. 단 한 번의 큰 조정이 오면, 투자자는 회복할 기회도 없이 강제 청산을 당할 수 있다.

역사적으로 훌륭한 투자자들도 레버리지로 인해 파산한 사례가 많다. 1998년 롱텀 캐피털 매니지먼트(LTCM) 는 노벨 경제학상을 받은 천재들이 운영한 펀드였지만, 과도한 레버리지로 인해 러시아 디폴트 사태에서 회복하지 못하고 붕괴했다. 2008년 금융위기 당시 리먼 브라더스 와 베어스턴스 같은 대형 금융기관들도 레버리지 의존도가 높아 결국 파산했다.

우리는 장기적인 투자를 하는 것을 염두해야 한다. 중간에 게임을 떠나게 되면 다시 돌아오기는 쉽지 않다.

시장은 예측할 수 없으며, 레버리지는 이를 더욱 위험하게 만든다.

주식 시장은 예측할 수 없는 방향으로 움직인다. 단기적인 조정(10~20{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374} 하락)은 언제든지 발생할 수 있으며, 레버리지를 사용하면 이런 조정에서도 심각한 타격을 입을 수 있다. 특히, 레버리지 투자자는 하락장에서 공포에 빠져 강제 청산당하는 경우가 많다.

2020년 코로나 팬데믹 초기, S&P 500은 단기간에 30{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374} 이상 급락했다. 레버리지를 사용한 투자자들은 대부분 청산당했으며, 이후 시장이 반등할 때도 다시 참여할 기회를 얻지 못했다. 레버리지는 상승장에서는 강력한 수단이지만, 하락장에서 투자자의 생존 가능성을 극단적으로 낮춘다.

레버리지는 감정적인 결정을 유발한다.

투자에서 감정을 배제하는 것은 성공의 핵심 요소다. 하지만 레버리지를 사용하면 투자자는 감정을 통제하기가 더욱 어려워진다. 레버리지를 사용하면 평소보다 훨씬 더 큰 금액이 투자되므로, 작은 가격 변동에도 심리적으로 극도의 불안감을 느끼게 된다. 주가가 조금만 하락해도 투자자는 손실을 확정 짓는 결정을 내릴 가능성이 커지고, 공포 속에서 비이성적인 매매를 하게 된다.

2021년 테크 버블 이후, 많은 개인 투자자들이 3배 레버리지 ETF(예: TQQQ, SOXL) 에 투자했다. 하지만 2022년 시장 조정이 오자, 대부분의 레버리지 ETF 투자자들은 심각한 손실을 입고 시장에서 퇴출되었다.

투자한 주식은 항상 장투해야하는가?

Should You Always Hold Stocks for the Long Term?

투자의 핵심 원칙 중에서도 복리(compounding) 는 가장 강력한 개념이다. 필립 피셔와 워런 버핏이 강조한 “최고의 기업을 찾아 오랫동안 보유하는 전략” 은, 현재의 버크셔 해서웨이가 유지하는 가장 효율적인 투자 방식이기도 하다.

하지만 버핏이 처음부터 장기 보유 전략을 사용한 것은 아니었다. 1950년대부터 1960년대까지 버핏은 벤저민 그레이엄의 단기 가치 투자 전략 을 사용하며 초기 자본을 빠르게 축적했다. 이후 찰리멍거와 함께 필립 피셔의 성장 투자(Growth Investing) 철학을 받아들이면서 점진적으로 장기 투자로 전환했고, 결국 버크셔 해서웨이를 인수한 후에는 기업의 장기적 성장을 극대화하는 초장기 보유 전략 을 확립했다.

1950~1960년대 버핏은 벤저민 그레이엄의 투자 원칙이 절대적이었다. 그레이엄은 “너무 싸게 거래되는 주식을 매수해, 가치가 정상화되면 매도” 하는 방식을 강조했다. 이 전략을 통해 버핏은 높은 수익률을 기록하며 빠르게 자본을 축적했다.

투자 방식

- P/B가 1 이하인 주식(즉, 장부가치보다 저렴한 주식) 매수

- 내재가치에 도달하면 즉시 매도(장기 보유보다는 가치 회복 후 매도)

특징 및 수익률

- 1950~1960년대 버핏의 연평균 수익률은 약 50{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374} 에 달했다.

- 당시 시장의 평균 수익률(베타)은 7{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374} 전후였으며, 버핏은 40{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374} 이상의 알파(초과수익)를 창출했다.

- 그러나 대부분의 투자 종목은 비교적 짧은 기간 동안 보유했다.

이 시기의 버핏은 철저히 저평가된 주식을 매수한 후, 정상적인 가치로 회복되면 매도하는 방식 을 사용했다. 즉, “오랫동안 보유하는 것”이 아니라, “저평가된 기업을 찾아 빠르게 차익 실현” 하는 전략이었다.

1960년대 중반부터 버핏은 단기 가치 투자 전략에서 점차 벗어나기 시작했다. 그가 깨달은 것은 “좋은 기업을 싸게 사는 것보다, 훌륭한 기업을 적절한 가격에 사서 오래 보유하는 것이 더 낫다” 는 점이었다.

왜 장기 보유 전략이 더 유리한가?

- 기업의 가치는 시간이 지남에 따라 증가할 수 있으며,

- 훌륭한 기업은 장기적으로 시장 수익률을 압도하는 복리 효과(compounding)를 제공하기 때문.

이후 버핏의 투자 철학에는 “좋은 회사를 찾으면 평생 보유하는 것이 최고의 전략이다.” 라는 개념이 자리 잡기 시작했다. 버크셔 해서웨이를 인수한 이후, 버핏의 투자 전략은 더욱 장기적인 접근 방식으로 변화했다.

버크셔 자체가 투자 회사가 되었기 때문에, 단기적인 가치 회복을 노리는 매매보다는 장기적인 기업 성장에 초점을 맞추는 방식 으로 투자 원칙이 바뀌었다.

변화된 투자 전략

- 훌륭한 회사를 발견하면 영원히 보유한다.

- 단기적인 주가 변동에 연연하지 않고, 기업의 본질적인 가치 상승에 집중

- 코카콜라, 애플, 아메리칸 익스프레스 같은 기업들을 수십 년간 보유

왜 버크셔는 장기투자하는가?

Why Does Berkshire Hold Investments for the Long Term?

장기간 우량한 기업을 투자하는 전략이 앞서 언급한 다양한 요소로 인해 우위라는 점을 제외하고도 버크셔의 장기 투자 전략은 나름의 이유가 있다고 생각한다. 일정 투자규모를 넘어서면 자금을 운용하는 방식은 달라져야 한다. 특히, 버크셔와 같은 규모에서는 더더욱 다양한 투자방식이 제한된다. 그래서, 소규모 자금을 운용하는 우리처럼 빠르게, 다양한 방식의 투자하는 방식을 취할 수 없다.

투자업에서 신뢰와 신용은 가장 중요한 자산이다. 버크셔는 규모가 커짐에 따라 빠르게 움직이기 어려운 한계를 가지지만, 그 대신 ‘장기적 파트너십을 보장하는 투자자’라는 이미지로 차별화된 경쟁력을 확보했다. 큰 자금을 보유한 것은 굉장한 경쟁력이지만 그런 자금력이 있는 투자자들은 세계적으로 다양하게 존재한다.

기업을 인수하고 매각하는 입장에서 보면 단기 수익을 목표로 하는 일반적인 재무적 투자자보다 장기적으로 회사를 보유하고 경영진과 협력할 투자자는 많지 않다. 그리고 그런 투자자에게 기업을 매각하고자 하는 니즈는 창업주 입장에서 더욱 강하게 존재한다. 특히, 버크셔는 인수 이후에 자회사로서 관리한다거나 경영에 참여한다거나 하지 않는다. 그런 부서나 직원도 존재하지 않는다.

막강한 자금력에 이러한 신뢰와 문화가 더해져 다른 투자자들이 접근하기 어려운 우량 기업과의 거래를 성사시킬 수 있다는 매우 큰 메리트가 존재한다. 그래서 버크셔는 장기적인 파트너십을 항상 강조한다. 내가 M&A 분야에 있으면서 느끼는 중요한 배움은 돈으로 모든 것을 해결할 수 없고, 이는 사람 간의 거래로서 “인간미”라는 부분이 굉장히 중요하게 작용한다는 점이다.

When I do something, I tend to first experience it by actually doing it. That said, when prior material exists, I try to take it in as fully as I can. In particular, if there is advice from someone who succeeded in circumstances similar to mine, or from someone who went before me, I make a point of following it. I tend to hold even more strictly to the “things not to do” they advise than to the “things to do.” Whatever choice I make, I value minimizing risk while still learning through experience in my own way.

For example, in my life there is no one whose conditions are exactly identical to mine. So even in situations with no clear answer, I tend to act first and to take on the challenge with courage. And even if I fail, I do not blame myself, because I think I have merely “erased one path that does not lead to success.”

Now let us take stocks as an example. When it comes to stock investing, countless people have already left behind their prior experiences and results in books and lectures. I think there is a great lesson to be drawn from this. Our economic system has advanced compared to 100 years ago. But when it comes to the act of trading stocks, I believe human nature has not changed by even 1%. Our reactions to investing, fear and greed, herd mentality, and irrational behavior are still being repeated. It is true, however, that thanks to technological progress, more investors now acquire information quickly and competition in the market has become fiercer. Yet that does not mean every investor makes wise choices. Rather than dismissing it with “the era we live in is different,” I think it is the wiser approach to observe and understand the behavior and environment of prior investors and to organize the patterns of behavior I should adopt for myself.

So when people around me start investing in stocks or in other forms, I recommend that they gradually expose themselves to the market through a minimum of knowledge (reading) along with a “test investment” (on the order of a few million won). This is not simply about making money; it is a process of understanding the world of investing.

What I am about to introduce is my own thinking about investing. This thinking is not something I created myself; it is a “replicated worldview” assembled from the ideas and principles of great investors and interpreted in my own way. As a child, I entered the world of investing by reading The Intelligent Investor, a book recommended by Warren Buffett. After that, through the writings and lectures of Benjamin Graham, Philip Fisher, Peter Lynch, Howard Marks, Charlie Munger, and Warren Buffett, I learned the fundamentals and, through my own experience, connected that knowledge organically. In that way, I am following their “Legacy.”

I have no children yet, but one of my dreams is that later, when my child is around the sixth grade, I want to explain investing to them in the same flow as this piece. I want to pass on the wisdom the great investors left behind and the countless failures I have experienced, in a way that helps reduce their mistakes a little. In that spirit, I have written down everything that I learned from various places such as books and interviews and that forms my foundation.

What I am about to introduce is the foundation and the entirety of my understanding of investing, learned indirectly from the great investors up to now.

What is Investing?

First, let us look at how the great investors define it.

Benjamin Graham

An investment operation is one which, upon thorough analysis, promises safety of principal and a satisfactory return. Operations not meeting these requirements are speculative.

Philip Fisher

Investment is about buying truly outstanding stocks and holding them for the long term.

Warren Buffett

Investing is laying out money now to get more money back in the future.

Charlie Munger

A great business at a fair price is superior to a fair business at a great price.

Howard Marks

The most important thing is to understand and control risk.

The investment philosophies of these five people are all different, but when it comes to “investing,” they all ultimately aim to deploy capital (the wealth one holds) effectively in order to create long-term wealth. It is quite intuitive and simple. I have nothing further to add to the definition.

Why Should You Invest?

When many people talk about investing, the first reason that comes to mind is probably “to make money.” Now I want to address economic structures beyond the goal of making money.

I believe that, economically, the two reasons below weigh very heavily in making investing essential.

First, because of inflation (rising prices), the value of money continuously declines.

If we simply leave money in the bank, its purchasing power shrinks as time passes. If 1,000 won from ten years ago is now worth only 800 won, then merely by doing nothing we are taking a loss.

Second, we must make use of a system in which money earns money, that is, the Compounding Effect.

As time passes, investment returns grow exponentially, and over the long term the wealth gap between someone who invested steadily and someone who did not widens uncontrollably. For example, if you invest for ten years at a 10% annual return, the principal grows 2.6 times. If you had invested 1 dollar in the S&P 500 in 1950, it would have become about 1,617 dollars by 2024.

In other words, not investing is not merely a loss of opportunity; it is like wasting time. We work every day to earn money, but if we learn how to make money work on its own, our lives can become far more comfortable.

Why Stocks Among Many Investment Options?

People considering investing have a variety of options. There are many investment assets such as real estate, bonds, and cryptocurrency, but over the long term I believe the most powerful investment asset is stocks. This is not simply a matter of returns; it is because of the intrinsic characteristics that stocks possess.

1. Stocks are an asset that can directly receive the benefits of economic growth.

When the economy grows, companies grow, and when companies grow, the value of stocks rises. Warren Buffett defined stocks as “an asset that can directly receive the benefits of economic growth.” This means that a stock is not merely a financial product but ownership of a part of a company.

By contrast, a bond is structured to pay a fixed amount of interest and is unrelated to a company’s growth. No matter how much a company grows, the bondholder receives only the promised interest. Stocks are different. As a company’s profitability grows, it invests with the cash accumulated within the company or pays dividends. And accordingly, the share price rises. You can directly enjoy the benefits of that growth. Therefore, a stock is a Productive Asset whose returns increase together with economic growth.

2. Stocks are an asset that can hedge against inflation.

Savings carry the problem that the value of money declines as time passes. When inflation persists, the amount of goods and services that can be bought with the same amount of money decreases. Real estate has an inflation-hedging function, but its investment efficiency can fall due to maintenance costs, taxes, and lack of liquidity.

By contrast, stocks are highly likely to naturally increase in value even in an inflationary environment, because companies can adjust their prices. When the prices of the products and services a company produces rise, this leads to higher revenue and is ultimately reflected in a higher company value. Through this mechanism, stocks become a powerful asset that can hedge against inflation over the long term.

3. Stocks can maximize the effect of Compounding

Compounding is the key factor that grows investment returns exponentially as time passes. Charlie Munger emphasized that “stock investors receive the benefits of compounding as time passes.” If you invest for ten years at an average annual return of 10%, the principal grows 2.6 times; after 20 years, 6.7 times; and after 30 years, 17.4 times. Bonds can also apply compounding, but because interest rates are low the effect is limited. In the case of real estate, there is rental income, but because maintenance and reinvestment costs are large, the compounding effect is relatively small.

Stocks are an asset that can maximize the compounding effect, because when a company’s profits increase the share price rises, dividends increase, and these are reinvested. In particular, when invested over the long term, the power of compounding becomes even stronger, which makes stocks an asset well suited to long-term investing.

4. Stock investing is not merely asset accumulation but a process of learning and growth.

Stock investing goes beyond being a means of making money; it offers investors the opportunity to understand the world more deeply. Philip Fisher said, “If you invest in great companies, you can learn and grow together with them.”

In the process of analyzing stocks, an investor comes to research particular industries and companies. For example, if you are interested in the automobile industry, you come to analyze companies such as Tesla, Toyota, and Hyundai, and through this your understanding of the flow of the automobile market and future technologies deepens. In the process of researching the fields one is interested in, such as the tech industry, healthcare, or consumer goods, an investor can cultivate insight into the economy as a whole.

Also, because holding a stock means owning a part of a company, you naturally come to understand how the company makes money and grows. This goes beyond simple asset accumulation and becomes a process of developing the ability to read the economy and the market. Therefore, it gives the investor an opportunity to grow. I think this is such an important factor that, had factor 4 not existed in investing, many of the great investors would have disappeared or been replaced by others.

What Kind of Investor Will You Be?

Investors fundamentally face the choice of whether to follow the market average or to try to beat the market. Depending on this choice, they can be divided into the Conservative Investor and the Aggressive Investor.

The conservative investor chooses Passive Investing. They accept the market return as it is and follow a strategy of maximizing the compounding effect over the long term.

By contrast, the aggressive investor chooses Active Investing. To beat the market, they analyze individual stocks and pursue an active trading strategy.

Benjamin Graham and Philip Fisher both distinguished between the defensive (conservative) investor and the aggressive investor, but the perspectives from which they viewed them differed. Graham distinguished investors with risk avoidance and safety at the center, while Fisher divided investors based on growth potential and long-term value creation.

Now, let us look at the difference between conservative and aggressive investing through these two perspectives.

Benjamin Graham: A typology of investors centered on risk management

Benjamin Graham emphasized that “the most important goal of investing is to prevent losses.” He divided investors into conservative investors (passive investors) and aggressive investors (active investors), and this distinction arose from differences in risk appetite and return expectations.

The Defensive Investor (Passive Investor, Conservative Investor)

The conservative investor prefers investments that are as safe as possible and tends to follow the market return as it is. They build a portfolio centered on assets with low volatility and stability.

Characteristics

– Protection of principal is the top priority

– Among undervalued stocks, prefers companies with high financial soundness

– A portfolio centered on bonds and dividend stocks (low equity weighting)

– Prefers investment methods that track an index, such as the S&P 500 ETF

– Sets a large Margin of Safety

– Avoids short-term volatility and maximizes the compounding effect over the long term

Representative strategies

– Index investing such as the S&P 500 ETF and the Dow Jones ETF

– Dividend-stock investing and increasing the weighting of bond holdings

– Investing centered on asset value, such as net worth and net current assets

The Aggressive Investor (Active Investor, Aggressive Investor)

The aggressive investor aims for returns higher than the market and actively seeks out and trades stocks. They do not merely look for undervalued stocks; they look for companies with high growth potential and expect high returns.

Characteristics

– Takes on a certain amount of risk for higher returns

– Invests not only in undervalued companies but also in companies growing faster than the market

– Has a strong interest in high-growth industries (tech, bio, etc.)

– Makes investment decisions by continuously researching company analysis and market trends

– Accepts short-term price volatility while selecting stocks with high intrinsic value through thorough analysis

Representative strategies

– Direct investment in individual stocks and active rebalancing

– Investing centered on growth industries (tech, bio, innovative companies)

– An aggressive bottom-buying strategy during market corrections

Philip Fisher: A typology of investors centered on growth potential

Philip Fisher divided investors from a different perspective than Benjamin Graham. He saw that the conservative investor who avoids short-term market volatility might in fact be more dangerous. Whereas Graham’s conservative investor mainly prefers stable dividend stocks, bonds, and blue chips, Fisher’s conservative investor was one who relied on past results and overlooked future growth potential.

The Conservative Investor (Passive Investor, Conservative Investor)

Characteristics

- Tries to avoid short-term volatility but is highly likely to miss long-term growth opportunities

- Prefers stable companies that pay dividends

- Places excessive importance on past results

- Gives insufficient consideration to a company’s R&D, innovation, and potential for market-share growth

- Highly likely to invest even in companies that lack technological innovation

The Aggressive Investor (Active Investor, Aggressive Investor)

Characteristics

- Does not merely look for undervalued companies but seeks out companies with high future growth potential

- Finds and holds great companies over the long term to maximize the compounding effect

- Thoroughly analyzes R&D, market-share growth, and management capability

- Is not swayed by short-term volatility and focuses on long-term growth potential

Representative strategies

- Invests in companies driving technological innovation

- Invests in companies with excellent management

- Prioritizes long-term growth potential over short-term price corrections

In the end, from Fisher’s perspective, the conservative investor risks missing big opportunities by clinging excessively to stability,

while the aggressive investor follows a strategy of accumulating wealth over the long term by recognizing a company’s growth potential.

So, now, what kind of investor will you be? First, let us look at the data.

Looking at the actual data, passive investing (the conservative investor) often records higher long-term performance than active investing (the aggressive investor). Many investors trade actively and try to find particular stocks in order to beat the market, but it is extremely rare for such strategies to succeed over the long term. By contrast, passive investors who simply follow the market record performance that beats most active investors.

According to the SPIVA (Active vs. Passive Investing) report, over a ten-year period 85 to 90% of active funds failed to beat the S&P 500. Analyzing data over a longer, 20-year period, more than 95% of active funds failed to outperform the index. In other words, it shows that even the majority of professional fund managers find it nearly impossible to beat the market consistently. The situation is not much different for individual investors.

According to the Dalbar Research report, over the past 20 years the average annual return of individual investors was only around 3 to 5%. Considering that the average annual return of the S&P 500 index over the same period was 8 to 10%, individual investors, far from beating the market, are in fact paying a considerable opportunity cost over the long term. This is the combined result of emotional trading, failed attempts at market timing, and excessive trading costs.

This data suggests an important fact. A conservative investor, simply by following a strategy of tracking the index, has a high likelihood of placing in the top 10 to 20% of all investors. Many investors struggle to beat the market, but maintaining a passive strategy is, with higher probability, more likely to guarantee success over the long term. Therefore, an individual investor who wants to maximize investment performance may find that, rather than going out of their way to outperform the market, the most efficient strategy is to enjoy the compounding effect steadily through passive investing.

Alpha (α) and Beta (β) theory from the perspective of market returns

When analyzing investment performance, the concepts of alpha (α) and beta (β) play an important role in understanding an investor’s disposition and strategy.

The passive investor aims to follow the market return as it is (β=1), while the active investor aims to generate returns in excess of the market (α>0).

1. Beta (β): the degree of movement together with the market

Beta (β) is an indicator of how closely a stock or portfolio moves in sync with the overall market. This is an important factor in assessing an investor’s risk appetite.

- β = 1 → the return of the stock (or portfolio) moves identically with the market.

- β > 1 → it shows greater volatility than the market. (e.g., if β = 1.5, when the market rises 10% the stock rises 15%)

- β < 1 → it has lower volatility than the market. (e.g., if β = 0.5, when the market rises 10% the stock rises 5%)

- β < 0 → an asset that moves in the opposite direction to the market (e.g., gold, some bonds)

For example, growth stocks such as Tesla and Netflix have a β greater than 1 (β > 1) and thus have greater volatility than the market. By contrast, defensive stocks such as Coca-Cola and P&G have a β less than 1 (β < 1) and thus have lower volatility than the market. The passive investor (conservative investor) generally chooses a strategy of tracking the overall market with a beta close to 1 (β ≈ 1).

This is a stable approach that follows the market return while not taking on excessive risk. By contrast, the active investor (aggressive investor) prefers high-beta (β > 1) stocks or tries to adjust the portfolio by taking advantage of market volatility.

2. Alpha (α): excess return (Active Return)

Alpha (α) refers to the degree by which a portfolio’s actual return exceeds the expected return of the market (or benchmark).

In other words, it is an indicator of whether the investment beat the market (Positive Alpha) or fell short of it (Negative Alpha).

Alpha (α) calculation formula:

α = actual return − (risk-free return + β × market return)

- α > 0 → recorded a higher return than the market → excess return (Positive Alpha)

- α = 0 → the same performance as the market

- α < 0 → recorded a lower return than the market → underperformance (Negative Alpha)

For example, if a fund manager records a higher return than the market, they have generated positive alpha (α > 0); conversely, if the market rose 10% but the portfolio rose only 8%, the alpha (α) is negative. The active investor aims to generate alpha (α) and strives to obtain returns in excess of the market.

However, considering the fact, mentioned earlier, that over the long term more than 95% of active funds fail to beat the market, you can see how difficult it is to generate alpha consistently. The passive investor does not aim to generate alpha. Instead, they choose a strategy that simply reflects the market return and focus on maximizing the compounding effect over the long term.

So, now is the moment of choice. Am I willing to take on the additional opportunity cost and invest my time to do active investing? Am I prepared to analyze financial statements, study industry trends, and study the market endlessly? In fact, even without the process of agonizing over investing and without any understanding of financial statements, you can earn sufficient returns simply through index investing. Going further, simply by investing in the index, you can over the long term achieve performance that beats most investors. So which choice is more efficient?

The answer depends on each individual’s disposition and goals. If, even after recognizing all of these facts, you still intend to make the effort to pursue alpha (α), then you may proceed to the next explanation. However, you must be sure to consider that the opportunity cost required in that process may be far greater than expected. You must not forget that active investing is not simply an investment but is more like a job.

Things to Bear in Mind to Become an Aggressive Investor

Active investing (aggressive investing) aims to generate returns in excess of the market (alpha, α). However, the “Opportunity Seeking Cost” that an investor must bear in order to do so is considerable.

This cost includes not only purely monetary costs but also time, psychological stress, and even the opportunity losses caused by mistaken judgment. The following organizes the main opportunity-seeking costs that an aggressive investor must bear.

1. Research Cost

Finding a good investment opportunity requires an enormous amount of time and effort. The aggressive investor does not simply follow the market; they must seek out individual stocks. This inevitably requires processes such as company analysis, industry research, review of financial statements, and comparison with competitors.

In this process, the investor takes on the following burdens.

- It takes a considerable amount of time to analyze a company’s earnings reports, 10-K (annual report), and financial statements.

- One must research the trends, competitive landscape, and innovation potential of a particular industry.

- One must continuously monitor market news, analyst reports, and investor conferences.

- The aggressive investor spends a lot of time looking for investment opportunities, but that cost does not guarantee excess returns.

2. Transaction Cost

The more trading there is, the more fees and taxes pile up. The aggressive investor tends to trade frequently in order to respond to market volatility. But frequent trading increases transaction costs and can cause larger-than-expected losses.

- Stock trading fees and Bid-Ask Spread costs arise

- Capital gains tax and transaction tax are imposed (in particular, the tax burden increases with short-term trading)

- The possibility that frequent trading continuously eats away at portfolio returns

- In particular, in the case of investors who use a high-frequency trading (commonly, day trading) strategy, transaction costs can surge, and it is not easy to generate enough excess return to overcome them.

3. Emotional Cost

The aggressive investor is always paying attention to the market and is under psychological pressure. The active investor must directly experience the market’s volatility, and this can bring emotional stress and psychological pressure.

- In a plunging market they engage in Fear Selling, or

- In a surging market they are highly likely to make irrational purchases out of the fear of missing out (FOMO, Fear of Missing Out).

- The burden of having to monitor the market all day long grows.

- Emotional stress is, in the end, highly likely to induce inefficient investment decisions.

- In particular, repeated emotional trading can become an obstacle to maximizing the long-term compounding effect.

4. Misjudgment Cost

You can be wrong no matter how hard you analyze. The active investor invests after predicting that a particular stock or industry will surge, but if that prediction is wrong they are highly likely to suffer a large loss.

- Predicting a company’s future growth is inherently difficult.

- Buying at the wrong timing (Timing Risk) can have a fatal impact on investment performance.

- They use complex strategies, yet may end up recording lower returns than simple index investing.

- In the end, no matter how outstanding an investor is, not all of their judgments can be correct,

- and as wrong investment decisions accumulate, they become more likely to suffer losses, far from beating the market.

5. Liquidity Risk Cost

If you invest in assets with low liquidity, it can be hard to convert them to cash when you need to. The aggressive investor often prefers stocks with low liquidity, such as high-growth industries, small- and mid-cap stocks, and new companies. But these assets carry the risk that they cannot easily be converted to cash when the market is poor.

- During a recession, even if you want to sell a stock, there may be a shortage of buyers.

- In certain industries (e.g., biotech, startups), there is a risk that liquidity drops sharply.

- There is a possibility that asset value plunges due to a sudden liquidity crisis.

- It can be hard to convert to cash when the market is poor.

6. Opportunity Cost of Capital

Investing aggressively can in fact result in lower performance than index investing. The aggressive investor selects individual stocks and expects high returns, but over the long term they are highly likely to record lower performance than index investing (S&P 500, ETFs).

- According to research, only 10 to 20% of investors beat the market over the long term.

- Most investors, while trying to beat the market, in fact record below-average performance.

What Are Stocks? How Should You View a Business?

This sentence said by Warren Buffett is not simply investment advice. It is a philosophical message that we must change our fundamental attitude toward investing. Many people see stocks only as “mere numbers, charts, and price movements.” But Buffett emphasizes that “a stock is not a mere ticker (symbol) but a part (ownership) of a real company.”

In other words, buying a stock is “not buying a number that seems likely to go up in the short term, but owning a part of an actually operating business.”

Let me give one example.

One day, I decided to start a small gimbap business. I would sell gimbap each morning in an area dense with offices. Every morning, I prepare fresh ingredients and make gimbap, and I sell it to office workers on their way to work. One roll of gimbap costs 1,000 won, and I can sell about 10 rolls a day. This way I generate revenue of 10,000 won a day, but the money that actually remains in my hands is different from the revenue.

To make gimbap, ingredient costs are needed. Buying basic ingredients such as rice, seaweed, eggs, spinach, and pickled radish costs 500 won per roll of gimbap. To make 10 rolls, 5,000 won in ingredient costs is needed. Also, to sell the gimbap I have to take the subway every day to move near the offices, which costs 100 won a day in transportation. Many of the customers who buy gimbap prefer to pay by card, so I also have to consider card payment fees. About 200 won a day in card payment fees arises.

Once all these costs are calculated, the money that remains in my hands each day, that is, the net profit, is 1,500 won. If I earn a net profit of 1,500 won a day, that is about 45,000 won in a month, and in a year (365 days) I can earn a net profit of about 547,500 won.

But I wanted to grow this business further. I wanted to expand the variety of gimbap and increase daily sales to 20 rolls, 30 rolls. To do that, however, initial capital was needed. Money was needed to buy more ingredients, and to do business in a good location I also had to consider rent. So I decided to recruit investors.

Recruiting investors means selling a part of my business. The investors invest money in my gimbap business, and in return they come to own a part of my business. So at what price would the investors want to buy the stock of my business?

If this business steadily generates a net profit of 540,000 won a year, then by simple calculation it can earn about 2.7 million won in profit over five years. So would investors be willing to buy this gimbap business for 2.7 million won? Or, seeing the possibility that the business grows further, might they pay a higher price?

But on the other hand, there is no guarantee that this business will necessarily succeed. What if people no longer buy gimbap? Or what if a competitor appears and sells gimbap that is cheaper and tastier than mine? What if ingredient costs rise and profits shrink? Considering these risk factors, investors will want to buy my stock cheaply.

This process is precisely the essence of stock investing. A stock is not a mere number but a process of understanding a real business and assessing its value. When buying a stock, an investor must not simply look at charts and numbers but analyze how the company makes money and whether it can grow in the future.

In the end, the question “which stock should I buy?” is the same as the question “which business do I want to own?” Buying a stock is not guessing at mere price movements but owning a part of a company. The investor must deeply understand how the company they invest in makes money, what growth potential it has, and what risks it carries. If we understand this principle, we will be able to make wiser investment decisions.

The following is an example Buffett gave in his shareholder letter.

“A bird in the hand is worth two in the bush”

Intrinsic value is a concept that has been discussed for a long time. In fact, the first person to put forward this concept could be said to be Aesop (the author of Aesop’s Fables). The maxim he spoke around 600 BC, “A bird in the hand is worth two in the bush,” captures its very essence.

In other words, certain money right now (the one bird in the hand) can be more valuable than uncertain money that may be obtained in the future (the two birds in the bush). What matters is finding the answers to questions such as: How certain are the future cash flows? How far away is that bush? How will future interest rates (the discount rate) change?

As we review countless companies, we assess how many birds (cash flows) each company can give us in the future. And it is the process of deciding which “bush to buy.”

The first question to ask when investing is not “Is this stock expensive or cheap?” Instead, you must consider, “What is the intrinsic value of this stock, and is it undervalued compared to the current market price?” In the stock market, Price and Value do not always coincide.

Warren Buffett said, “Price is what you pay, and value is what you get.” In other words, there is a belief that price is shaken in the short term by the market’s emotions and psychology, but over the long term a company’s intrinsic value is reflected in the share price. Therefore, an investor must not simply buy because the current price looks cheap, but must analyze whether the company is trading at a price below its intrinsic value.

What Is Intrinsic Value?

What is Intrinsic Value?

Intrinsic value is the real value that an asset essentially possesses. – Warren Buffett

Benjamin Graham did not define intrinsic value mathematically and precisely, but the concept is close to the philosophy that “you should evaluate a company in the same way you would buy a private business.” Intrinsic value can be defined not as mere share-price movement but as the present value of all the cash flow a company earns.

In other words, if we could perfectly predict the future, the intrinsic value would be all the money the company will earn going forward converted into present value. But because it is realistically impossible to predict the future 100%, investors use various methods to estimate intrinsic value.

The difference between intrinsic value and market price

A company’s intrinsic value and the share price at which it trades in the market do not always coincide. For that reason, an investor must take the strategy of buying when a company is trading at a price below its intrinsic value and waiting until it reaches its intrinsic value.

Characteristics of Intrinsic Value

- An objective value determined by comprehensively evaluating a company’s held assets, profit-generating ability, cash flow, and growth potential

- An essential value that does not change with the market’s emotions (fear and greed)

Characteristics of Market Price

- A price that fluctuates in real time in the stock market

- A number that swings sharply according to investor psychology, supply and demand, news, and changes in interest rates

- The market forms prices emotionally in the short term, but over the long term the price is adjusted to match the company’s results and intrinsic value.

When analyzing companies, investors can broadly take two perspectives.

First, the method of thoroughly analyzing a company’s current financial condition and intrinsic value to find undervalued stocks.

Second, the method of analyzing a company’s qualitative factors and long-term growth potential to find companies that will grow greatly in the future.

The figures who represent these two approaches are precisely Benjamin Graham and Philip Fisher. Graham emphasized thorough, numbers-based analysis, while Fisher placed importance on a company’s qualitative factors and growth potential. The two men’s investment philosophies are different, but they were identical in the point that “investing is a process of comparing the current price with future value.” Nevertheless, which method is better still depends on the investor’s choice. To borrow Buffett’s example, where Ben Graham focused on whether birds really existed inside the bush, Phil Fisher considered it important how much the birds inside that bush would increase.

Graham vs. Fisher: which approach is better? Graham’s and Fisher’s investment philosophies differ greatly, and it is difficult to conclude that either one is absolutely right. But the prevailing view seems to be that, as has been demonstrated in many respects, Ben Graham’s method is hard to apply in large-scale investing.

At first I was strongly influenced by Benjamin Graham and placed importance on quantitative factors. But Charlie Munger told me that this alone was not enough. He said he had learned more from studying law than from studying finance, and he emphasized that in investing too one should give more consideration to qualitative factors. As a result, I realized that Charlie and Philip Fisher’s view was right.

Warren Buffett

Discount Rate

When deriving intrinsic value, I mentioned the part about “interest.” In calculating future cash into present value, the interest rate is very important. To explain the discount rate as it is used in the area I am responsible for at work, it is very complex, but setting aside the difficult explanation for now, many people often ask Warren what percentage discount rate he uses. The answer is as follows.

When we assess intrinsic value, we set the discount rate based on the long-term risk-free rate (that is, the government bond rate). This is a method of converting a company’s future cash flows into present value, using the yield of a safe investment asset (e.g., U.S. Treasuries) as the benchmark.

Warren Buffett

But I think the important takeaway is not simply that he uses the long-term U.S. Treasury rate. The truly important point is that we should give weight to a remark like the following.

We simply look for “one-foot bars” that we only need to step over and step over them. We do not have the ability to jump over seven-foot bars, but at the very least we can judge “whether this bar is one foot or seven feet.”

Warren Buffett

The way I think about how Berkshire derives intrinsic value is this: it does not make decisions where the answer goes back and forth ambiguously by finely adjusting the discount rate. At a past shareholders’ meeting, Buffett said that while he holds the method of a DCF calculation in his head, no staff member (employee) actually computes it. What we should think about is not whether Warren applies an 8% discount rate or a 9% one, but that the point is to stay away from such decisions.

Example of Intrinsic Value Calculation Methods

The following is the way Warren Buffett explained most concretely, during a shareholders’ meeting, how to derive intrinsic value. I have organized it here. I think he taught a more concrete framework for calculating intrinsic value than any other famous investor.

An intrinsic value assessment method using a farm as an example: suppose we are trying to buy a farm.

- From our research, we found that an acre can produce 120 bushels of corn or 45 bushels of soybeans.

- We know the fertilizer costs, property taxes, the labor cost we would pay the farmer, and so on.

- Calculating this conservatively, we assume that, from the owner’s standpoint, we can earn 70 dollars per acre while doing nothing.

So how much should we pay for this 70 dollars of income per acre?

- Will agricultural productivity gradually improve?

- Will the prices of agricultural products rise?

We must consider such factors conservatively.

Now, we must set a target return.

- If we want a 7% return, we can pay 1,000 dollars per acre.

- If the farmland price is 900 dollars per acre, we would consider buying.

- On the other hand, if it is 1,200 dollars per acre, we would look for another investment opportunity.

We evaluate a company like a “Corporate Farm.” When we evaluate a company, we use the same approach as when evaluating a farm. To do so, we must assess the following.

- The company’s Competitive Position

- Can this company maintain its edge in the market going forward?

- The Dynamics of the Business

- What changes will this industry undergo over the long term?

- The Outlook for the Future

- How far into the future can we see?

However, for some companies it is nearly impossible to predict the future. We must take as investment targets only those companies whose future we can be relatively certain about.

Which Company Should You Invest In?

The most central question when evaluating a company is: when and how much cash will come back to me from the cash I put in? Whether you buy Tesla, McDonald’s, NVIDIA, or any company, the essence of investing ultimately lies in predicting cash flows and appropriately assessing the price for them. When viewing a company as a single asset, the most important factors are as follows.

- Is additional capital injection needed?

- From when does cash start to flow in?

- What is that cash worth now? (What is the appropriate discount rate?)

Only by finding the answers to these three questions can you make a rational decision as an investor.

A company’s cash flow is just like the interest on a bond. The cash flows a company will earn going forward play a role similar to the interest on a bond. In the case of a bond, the investor invests a certain amount and, in return, receives a fixed amount of interest over a set period.

But a company differs from a bond in that the investor must directly predict the future cash flows themselves. If a company’s future earnings are stable, that company will behave like a bond with a fixed rate. By contrast, if a company’s future cash flows are uncertain, it becomes an investment target for which the investor must take on additional risk.

We must invest only in companies whose business we understand and can predict. The key to investing is not simply “Is this a good company?” It is more important to analyze “Will this company continue to generate steady cash flows going forward?”

We cannot precisely calculate the intrinsic value of every company. But for companies we understand well, we can estimate an approximate range. In other words, our goal is not to derive a perfect number but to make investment decisions within a reasonable margin of error.

- Does a company have the potential to continuously generate profits even 10 or 20 years from now?

- Is its cash flow steady and predictable?

- To what extent can an investor trust the company’s future?

Looking at Warren Buffett’s investment portfolio, there are many brand and consumer-goods companies. He has at times spoken about why he acquired them. He explains the reasons he invested as follows.

Gillette razor blades: They hold 70% of the global razor market. Even 100 years from now they will still be a powerful brand. How a razor blade is made, where they buy the steel, how distribution is done, are all known facts, but the reason they still hold 70% is that people do not easily switch brands.

Coca-Cola: 19 billion cases are sold a year. Will people still drink Coca-Cola 10 years from now? I would stake my life on the answer to this question.

See’s Candy: 35 million people live in California. Most of them have a memory of See’s Candy. In the chocolate market, Snickers was number one 10 years ago and number one 20 years ago as well. People do not easily switch their chocolate.

How to Make Investment Decisions?

Charlie Munger

We do not need to evaluate every company

We do not have a system that can evaluate every company.

Most companies are too complex or too hard to predict,

so we put almost every company in the “Too Hard” basket and simply give up.What we do is a process of filtering out the simple ones.

That is, finding a few investment opportunities that we can judge easily.If you want “the ability to evaluate every investment opportunity precisely,” we cannot offer that kind of help.

Investing is the process of considering all opportunities and making the choice most suitable for oneself. At Berkshire’s shareholders’ meetings and at investors’ lectures, the question “How do you derive intrinsic value?” never fails to come up. Many people expect that there must be a simple formula that lets you solve investing like a math problem. But I imagine that great investors such as Warren Buffett, Charlie Munger, and Howard Marks must have felt frustrated whenever they received this question.

Because I think intrinsic value is not a mere number but the result of complex thinking. Many people want a “precise number” in investing. But in reality, it is impossible to derive intrinsic value with a single precise formula.

- Intrinsic value must comprehensively consider many factors, such as a company’s current earnings, future growth potential, economic Moat, the capability of management, and the market environment.

- Indicators such as DCF (discounted cash flow), P/E, and P/B are merely reference material; they do not provide an absolute answer.

- Blind faith in mathematical models can in fact be dangerous in investing.

“There is no perfect model. But a roughly right model is better than a completely wrong one.”

John Maynard Keynes

As Keynes said, investors too must admit that there is no perfect model. Investing is a process of dealing with uncertainty, and what matters is not arriving at a precise answer but making “the most reasonable judgment.” Our goal is not a complex formula but having a complex way of thinking. If there were a formula to derive intrinsic value mathematically, everyone would become rich. But reality is not so. Investing is not a simple equation but the result of decision-making based on logical thinking and experience.

When Should You Invest?

When it comes to stock market cycles, I think Howard Marks’s explanation is the most fitting. In particular, Howard interprets the stock market through human psychology rather than financial factors.

The stock market is driven by emotion. Greed and fear distort investors’ judgment, and when these two emotions run to extremes the market overheats or slumps. When most investors are optimistic, the market has likely already reached a peak; conversely, when everyone is pessimistic, there are many undervalued opportunities. Therefore, an investor must go against the herd mentality and maintain a cool-headed attitude when the market moves emotionally.

When to be cautious about investing: when herd mentality is excessively optimistic

When the market overheats, investors take on an irrationally optimistic attitude. Wariness toward investing disappears, and everyone jumps into the market. The belief spreads that the stock market will keep rising in the short term, and investors do not consider a margin of safety.

The features of a period when herd mentality is excessively optimistic share several things in common.

First, market participants surge. Interest in stock investing rises, and inexperienced individual investors actively jump into the market. An atmosphere forms in which “everyone is making money,” and you start to hear “now is the opportunity” said frequently around you.

Second, the logic of “this time is different” appears. Existing investment principles are ignored, and the claim arises that a new paradigm dominates the market. During the past dot-com bubble there was the logic that “internet companies do not need profits,” and during the real estate bubble the belief spread that “real estate prices never fall.”

Third, share prices surge regardless of corporate results. Even companies that are not making profits are granted high valuations, and expectations rather than results drive prices up. When the market ignores basic company analysis and focuses only on short-term momentum, a bubble is highly likely to form.

Fourth, investors are seized by FOMO (Fear of Missing Out). In the news and on social media, the message “if not now, it will be too late” spreads, and people are easily swept up even by unverified information.

Finally, leverage increases excessively. More people invest with borrowed money, and margin trading explodes. When the market is rising, large profits can be made, but once it starts to fall, rapid liquidations occur and market volatility grows.