최근 읽은 하워드 막스의 메모 중 눈길이 갔던 것은 “On Bubble Watch”이다. 하워드 막스는 25년 전, ‘버블닷컴(bubble.com)’이라는 글을 통해 당시 닷컴 열풍을 ‘버블’로 진단하며 경각심을 불러일으킨 바 있다. 1999~2000년대 인터넷·전자상거래·테크 기업들에 대한 과도한 낙관을 경계했고, 그의 예상대로 수많은 인터넷 기업이 2000년대 초반 폭락했다.

주식시장이 고점인지 저점인지 명확하게 단정할 수는 없지만, 주식시장만큼 역사를 쉽게 잊어버리는 곳도 없다. 한국에서는 주식투자가 대중화된 지 오래되지 않았지만, 미국은 100년 가까운 역사를 가지고 있다. 과거에도 지금과 유사한 패턴이 반복됐고, 많은 사람들은 그 사실을 잊은 채 같은 실수를 반복하곤 했다.

메모의 도입부 중 “Being too far ahead of your time is indistinguishable from being wrong”이라는 문장이 인상적이었다. 한국어로 옮기자면 “시대를 너무 앞서가면, 그건 틀린 것과 구분하기 어렵다” 정도가 된다. 지나치게 앞서가다 보면 결국 시점이 맞지 않아 틀린 것으로 보일 수 있다는 뜻이다. 그의 의견이 맞을지 틀릴지는 모르지만, 적어도 25년 전 버블닷컴에서는 틀리지 않았다.

하워드는 오크트리 인사이트(Insights)를 통해 투자자들에게 지속적으로 시장에 대한 의견을 공유해 왔다. 가치투자자로서 전설적인 위치에 있는 그가 다시 ‘버블’이라는 주제를 꺼낸다는 것에 어떤 의미가 있을지를 다시 생각해보게 된다. 물론, 그가 버블을 언급했다고 해서 반드시 지금 시장이 버블이라는 의미는 아니다. 하지만 시장이 과열될 가능성을 염두에 두고 대비하는 자세는 필요할 수 있다.

나는 가치투자자들을 좋아한다. 하워드 막스의 책을 읽다 보면 흥미로운 부분들이 많다. 그는 시장을 분석할 때 단순히 수치적인 요소만 보는 것이 아니라, 심리적인 요소도 함께 고려한다. 군중심리, 투자자의 감정, 그리고 매수·매도 타이밍에서의 심리적 함정까지 깊이 다룬다. 결국 투자를 잘하고 못하는 것도 자기 절제와 심리에 달려 있다고 생각한다. 이런 부분을 깊이 있게 설명하는 걸 보면, 시장과 투자자들에 대한 그의 이해도가 상당하다는 걸 알 수 있다.

하워드 막스의 대표적인 저서 두 권을 추천한다. 시간이 된다면 한 번쯤 읽어보는 것도 좋을 것이다. 시장을 보는 관점, 투자자의 심리, 그리고 장기적인 투자 철학을 배우는 데 도움이 될 것이다.

- The Most Important Thing (투자에 대한 생각)

- Mastering the Market Cycle (하워드 막스 투자와 마켓 사이클의 법칙)

결국 투자는 정답이 없는 영역이다. 다만 역사를 잊지 않고, 심리에 휩쓸리지 않는다면 보다 현명한 선택을 할 수 있을 것이다. 그런 점에서 하워드 막스의 메모는 시장을 바라보는 데 있어 많은 시사점을 가지고 있다.

1. 버블을 구성하는 핵심 요소

막스는 버블을 “가격 급등”이 아닌, “투자자 심리의 극단”으로 정의한다. 즉, “이 자산은 너무나 뛰어나기에 아무리 비싸도 된다”라는 인식이 폭넓게 퍼질 때가 진정한 버블 국면이라고 말한다. 그가 메모에서 언급한 구체적 요소들은 다음과 같다.

새로운 테마와 “이번에는 다르다”는 믿음

- ‘The New, New Thing’: 투자자들은 첨단 기술(AI, 인터넷 등)이나 새로운 금융 상품 등에 “역사적 비교가 무의미하다”며 높은 가치를 부여한다.

- “이번에는 다르다”: 과거 평가 잣대가 통하지 않는다고 믿고, 기존 P/E나 수익성 대신 미래 비전과 희망적 지표(예: 페이지뷰, 트래픽)를 근거로 투자 결정을 내린다.

극단적 낙관과 공포(FOMO)

- “나만 빠지면 손해다”라는 FOMO(Fear of Missing Out) 심리가 확산되면, 위험 신호에도 불구하고 군중이 몰린다.

- 막스는 과거 닷컴버블 당시 “인터넷 회사를 안 사면 뒤처진다”는 두려움이 시장 전반에 만연했다고 언급한다.

검증되지 않은 가치평가 방식

- Nifty Fifty 시절(1960년대 말부터 1970년대 초까지의 시기에서 미국의 투자자들이 가장 선호한 50개의 종목)에는 일부 기업들이 P/E 60~90배로 거래되기도 했다. 닷컴 시절에는 “수익이 없지만 미래엔 잘될 것”이라는 논리만으로 고평가 되었다.

- 막스는 “가격(Price)과 가치(Value)의 괴리”가 커져도 투자자들이 이를 무시하고 매수에 뛰어든다면, 이미 버블 단계일 수 있다고 본다.

“가격은 중요치 않다”는 심리

- “이 기업은 너무 좋은 회사니까 아무리 비싸도 괜찮다”는 생각은 투자의 기본 원칙(싸게 사서 비싸게 판다)을 잊게 만든다.

- 막스는 “좋은 기업도 지나치게 비싸게 사면 위험해지고, 평범한 기업도 충분히 싼 가격에 사면 매력적”이라고 강조한다.

2. 과거 사례: 반복되는 거품

하워드 막스는 「On Bubble Watch」에서 “버블은 늘 ‘새로운 무언가’가 등장할 때 반복된다”라고 말하며, 대표적인 사례로 다음을 든다.

- Nifty Fifty (1960~70년대) IBM, 코카콜라, 제록스 등 당대 최고의 50개 기업에 “아무리 높은 가격이라도 사고 보자”는 맹신이 있었다. 그러나 1973~74년 시장 급락 시 90{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374}에 가까운 손실을 입은 사례까지 발생했다. “가격 무시는 위험하다”는 교훈을 남겼다.

- 닷컴(TMT) 버블 (1990년대 후반 ~ 2000년 초) 인터넷이 세상을 바꿀 것이라는 확신이 번지면서 “실적 없는 기업도 상장만 하면 주가가 폭등”했다. 막스가 “버블닷컴”으로 경고했고, 2000~2002년 폭락 후 다수의 기업이 소멸했다.

- 서브프라임(주택) 버블 (2000년대 중반) “미국 집값은 절대 안 떨어진다”는 믿음으로 대출 규제가 사라지고, 소득 증명도 안 되는 대출까지 무분별하게 발급됐다. 결국 2008년 글로벌 금융위기로 이어졌고, 시장은 큰 고통을 겪었다.

3. 지금 시장, 과연 버블인가?

Magnificent Seven과 집중 현상

막스는 최근 S&P 500에서 상위 7개 빅테크 기업(애플, 마이크로소프트, 알파벳, 아마존, 엔비디아, 메타, 테슬라)이 시가총액의 32~33{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374}를 차지한다는 점을 주목한다. 이는 과거 TMT 버블 시기(22{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374})를 상회하는 수준으로, 특정 소수 종목에 대한 쏠림이 심해진 상태라는 것이다.

글로벌 시가총액 편중

미국 주식시장의 전체 가치가 전 세계(MSCI World 지수)에서 차지하는 비중이 70{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374}에 달한다는 점도 언급한다. 막스는 “미국이 세계 경제를 이끌 만큼 강하긴 하지만, 이렇게 높은 비중은 과거에도 드물었다”라고 지적한다.

“아직 버블인지 단정 못 하겠다”

- 막스는 자신이 크레디트(채권) 투자자이므로, 주식이나 테크 기업을 직접 분석하진 않는다고 선을 그으면서도, “심리적 과열 징후가 보인다”라고 말한다.

- 다만 “대형 기술주는 실제로 수익 모델이 견고하고, P/E가 60~90배에 달했던 Nifty Fifty 수준은 아니다”라는 반론도 함께 제시한다.

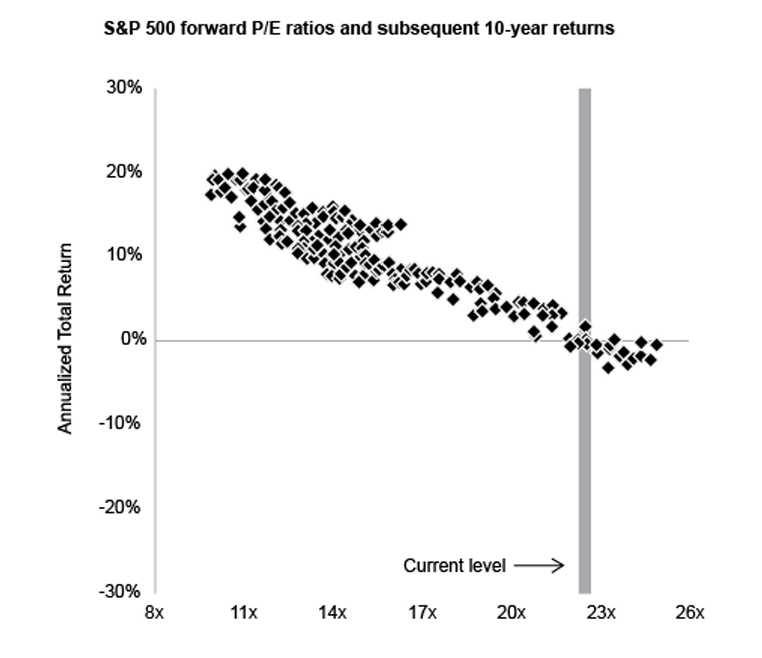

멀티플 그래프와 시사점

막스는 메모 말미에서 JP모건 자산운용(J.P. Morgan Asset Management)이 만든 S&P 500의 Forward P/E(미래 주가수익비율)와 향후 10년간 연평균 수익률 간 상관관계 그래프를 인용한다. 이 그래프를 통해 시장이 버블에 가까운 상태인지 엿볼 수 있다고 강조한다.

- Forward P/E가 높을수록 향후 수익률은 낮다. 1988~2014년의 월별 데이터를 보면, P/E가 높았던 구간에서 S&P 500의 향후 10년 연평균 수익률이 대부분 낮게 나타났거나 심지어 음(-) 수였다. 반대로 P/E가 낮았던 구간은 이후 10년간 양호한 수익률을 기록했다.

- 2025년 초 기준, S&P 500 Forward P/E 약 22배이다. 막스는 “P/E 22배 수준이면 과거 통계상 10년 후 연평균 수익률이 대략 +2{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374} ~ -2{61dd6028939e6e9509497ea9515dd6fa0e1cd722d4bf42155a61f48a59c57374}”를 오갔다고 지적한다. 이는 “이미 높은 기대치가 시장에 반영되어 있고, 작은 악재에도 가격 조정이 크게 올 수 있다”는 뜻으로 해석된다.

- 장기 투자자에게 던지는 시그널 10년간의 평균 수익률이 낮을 수 있다는 것은, 단순히 “단기 폭락이 온다”는 결론은 아니지만, “이익 성장 대비 주가가 너무 앞서가는 상태”를 의미할 수 있다. 특히 레버리지를 크게 쓰는 투자자는 고평가 국면에서 갑작스러운 조정이 오면 타격이 클 수 있음을 시사한다.

4. 결론: 버블은 되풀이되지만, 대비는 가능하다

하워드 막스는 25년 전 ‘버블닷컴’ 메모에서 이미 “투자자들의 맹목적 믿음과 극단적 군중심리”를 경고했고, 닷컴버블 사태는 이를 여실히 증명했다. 이번 메모에서도 그는 “지금 당장 버블이라고 확언할 순 없지만, 시장이 과열 국면으로 치닫는 징후들을 무시하기 힘들다”라고 말한다.

- 심리적 관점: “이번에는 다르다”는 낙관론이 팽배해지고, “가격이 중요치 않다”는 분위기가 자리 잡으면 그때가 바로 버블의 정점일 가능성이 크다.

- JP모건 멀티플 그래프: Forward P/E가 22배 안팎으로 높아진 것은, 향후 10년간 수익률이 과거 평균에 크게 못 미칠 수 있음을 시사한다.

- 역사적 순환: Nifty Fifty, 닷컴, 서브프라임 등 버블은 그 형태만 다를 뿐 기본 메커니즘은 반복되어 왔다.

따라서 투자자는 분산 투자, 냉정한 가치 평가, 그리고 “가격과 가치의 괴리”가 커질 때 의심을 품는 태도가 필요하다. 매번 거품이 형성될 때마다 “열광은 오래가지 않지만, 그 후폭풍은 길게 간다”라고 경고한다. 버블을 완벽히 피하는 건 어렵더라도, 이를 경계하고 스스로 리스크를 관리하는 것은 분명 우리 몫이다.

원문 : On Bubble Watch

One of the Howard Marks memos I read recently that caught my eye was “On Bubble Watch.” Twenty-five years ago, Marks wrote a piece called “bubble.com” in which he diagnosed the dot-com mania of the time as a ‘bubble’ and raised the alarm. He warned against the excessive optimism surrounding internet, e-commerce, and tech companies in the 1999–2000 era, and just as he predicted, countless internet companies collapsed in the early 2000s.

We can never say for certain whether the stock market is at a top or a bottom, but there is no place that forgets history as easily as the stock market. Stock investing became widespread in Korea only fairly recently, but in the United States it has nearly a hundred years of history. Patterns similar to today’s have repeated in the past, and many people, forgetting that fact, have tended to repeat the same mistakes.

One sentence in the memo’s introduction struck me: “Being too far ahead of your time is indistinguishable from being wrong.” Rendered into Korean, it comes out roughly as “if you get too far ahead of your time, it’s hard to tell apart from being wrong.” The point is that if you run too far ahead, your timing ends up off and you can look like you were simply wrong. Whether his view turns out to be right or wrong, no one knows—but at least with bubble.com twenty-five years ago, he was not wrong.

Through Oaktree’s Insights (Insights), Howard has continually shared his views on the market with investors. It makes me think again about what it might mean that someone in his legendary position as a value investor is once more bringing up the subject of a ‘bubble.’ Of course, the fact that he mentions a bubble does not necessarily mean the market is one right now. But it may be worth keeping the possibility of an overheated market in mind and preparing for it.

I like value investors. Reading Howard Marks’s books, I find many parts fascinating. When he analyzes the market, he looks not only at the numerical factors but also considers psychological ones. He delves deeply into crowd psychology, investor emotion, and the psychological traps around the timing of buying and selling. In the end, I think whether one invests well or poorly also comes down to self-discipline and psychology. Seeing him explain these aspects in such depth, you can tell how deep his understanding of the market and of investors really is.

I recommend two of Howard Marks’s signature books. If you have the time, they are well worth reading. They will help you learn how to view the market, understand investor psychology, and develop a long-term investment philosophy.

- The Most Important Thing

- Mastering the Market Cycle

In the end, investing is a domain with no single correct answer. But if we do not forget history and are not swept along by psychology, we can make wiser choices. In that sense, Howard Marks’s memo offers plenty of food for thought when it comes to viewing the market.

1. The core elements that make up a bubble

Marks defines a bubble not as a “surge in prices” but as an “extreme of investor psychology.” In other words, he says the true bubble phase is when the perception that “this asset is so wonderful that no price is too high” spreads widely. The specific elements he mentions in the memo are as follows.

A new theme and the belief that “this time is different”

- ‘The New, New Thing’: Investors assign high valuations to cutting-edge technology (AI, the internet, etc.) or new financial products, claiming that “historical comparisons are meaningless.”

- “This time is different”: Believing that past valuation yardsticks no longer apply, they base investment decisions on future visions and hopeful metrics (e.g., page views, traffic) instead of conventional P/E or profitability.

Extreme optimism and fear (FOMO)

- When the FOMO (Fear of Missing Out) mentality of “I’ll lose out if I’m the only one left behind” spreads, the crowd piles in despite warning signs.

- Marks notes that during the past dot-com bubble, the fear that “if you don’t buy internet companies you’ll fall behind” was pervasive across the market.

Unproven valuation methods

- In the Nifty Fifty era (the fifty stocks most favored by U.S. investors from the late 1960s through the early 1970s), some companies traded at P/E ratios of 60–90x. In the dot-com era, companies were overvalued on the sole logic that “they have no earnings now, but they’ll do well in the future.”

- Marks holds that even as the “gap between price and value” widens, if investors ignore it and rush in to buy, it may already be the bubble stage.

The mindset that “price doesn’t matter”

- The thought that “this is such a great company that it’s fine no matter how expensive it is” makes investors forget the basic principle of investing (buy low, sell high).

- Marks emphasizes that “even a good company becomes risky if you buy it at too high a price, and even an ordinary company is attractive if you buy it cheaply enough.”

2. Past cases: recurring bubbles

In “On Bubble Watch,” Howard Marks says that “bubbles always recur whenever some ‘new thing’ appears,” and he cites the following as representative cases.

- Nifty Fifty (1960s–70s): There was a blind faith in the fifty greatest companies of the day—IBM, Coca-Cola, Xerox, and others—that “you should just buy them no matter how high the price.” Yet when the market plunged in 1973–74, there were even cases of losses approaching 90%. It left the lesson that “ignoring price is dangerous.”

- The dot-com (TMT) bubble (late 1990s to early 2000): As the conviction that the internet would change the world spread, “even companies with no earnings saw their share prices soar simply by going public.” Marks warned of it with “bubble.com,” and after the 2000–2002 crash many companies vanished.

- The subprime (housing) bubble (mid-2000s): On the belief that “U.S. home prices never fall,” lending regulations disappeared, and even loans with no income verification were issued indiscriminately. It ultimately led to the 2008 global financial crisis, and the market endured great pain.

3. Is the market today really a bubble?

The Magnificent Seven and concentration

Marks points out that recently, the top seven big-tech companies in the S&P 500 (Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, Tesla) account for 32–33% of the index’s market capitalization. This exceeds the level seen during the past TMT bubble (22%), indicating that concentration in a handful of specific stocks has become severe.

Concentration in global market capitalization

He also notes that the total value of the U.S. stock market accounts for as much as 70% of the entire world (the MSCI World index). Marks observes that “the U.S. is indeed strong enough to lead the global economy, but a share this high has rarely occurred even in the past.”

“I can’t yet say for certain whether it’s a bubble”

- Marks draws a line, noting that since he is a credit (bond) investor, he does not directly analyze stocks or tech companies—yet he says “there are signs of psychological overheating.”

- At the same time, he also offers the counterpoint that “the large-cap tech stocks actually have solid earnings models and are not at the Nifty Fifty level, where P/Es reached 60–90x.”

The multiple chart and its implications

At the end of the memo, Marks cites a chart created by J.P. Morgan Asset Management showing the correlation between the S&P 500’s Forward P/E and the average annual return over the subsequent ten years. He emphasizes that this chart offers a glimpse of whether the market is in a state close to a bubble.

- The higher the Forward P/E, the lower the subsequent return. Looking at monthly data from 1988 to 2014, in the periods when the P/E was high, the S&P 500’s average annual return over the following ten years was for the most part low, or even negative. Conversely, periods when the P/E was low recorded solid returns over the next ten years.

- As of early 2025, the S&P 500’s Forward P/E is about 22x. Marks points out that “at a P/E level of 22x, statistically the average annual return ten years out has historically ranged from roughly +2% to -2%.” This can be read to mean that “high expectations are already priced into the market, and even minor bad news could trigger a large price correction.”

- The signal it sends to long-term investors: the fact that the average return over ten years could be low does not simply lead to the conclusion that “a short-term crash is coming,” but it may mean a state in which “share prices have run too far ahead relative to earnings growth.” In particular, it suggests that investors who use a lot of leverage could be hit hard if a sudden correction comes during an overvalued phase.

4. Conclusion: bubbles recur, but you can prepare

Twenty-five years ago, in his “bubble.com” memo, Howard Marks already warned of “investors’ blind faith and extreme crowd psychology,” and the dot-com bubble proved it in full. In this memo too, he says, “I can’t declare right now that it’s a bubble, but it’s hard to ignore the signs of a market hurtling toward an overheated phase.”

- Psychological perspective: when the optimism of “this time is different” becomes rampant and an atmosphere of “price doesn’t matter” takes hold, that is most likely the peak of the bubble.

- J.P. Morgan multiple chart: the Forward P/E rising to around 22x suggests that returns over the next ten years could fall well short of the historical average.

- Historical cycle: the Nifty Fifty, the dot-com era, subprime—bubbles differ only in form, but the basic mechanism has repeated.

Investors therefore need diversification, cool-headed valuation, and an attitude of skepticism when the “gap between price and value” widens. Every time a bubble forms, he warns that “the euphoria does not last long, but the aftermath lingers.” Even if it is hard to avoid bubbles perfectly, guarding against them and managing our own risk is clearly up to us.

Original: On Bubble Watch

댓글을 남기려면 이메일로 가입/로그인해주세요. Sign in with your email to leave a comment.